Blank Dte 100 Ohio Template

Blank Dte 100 Ohio Template

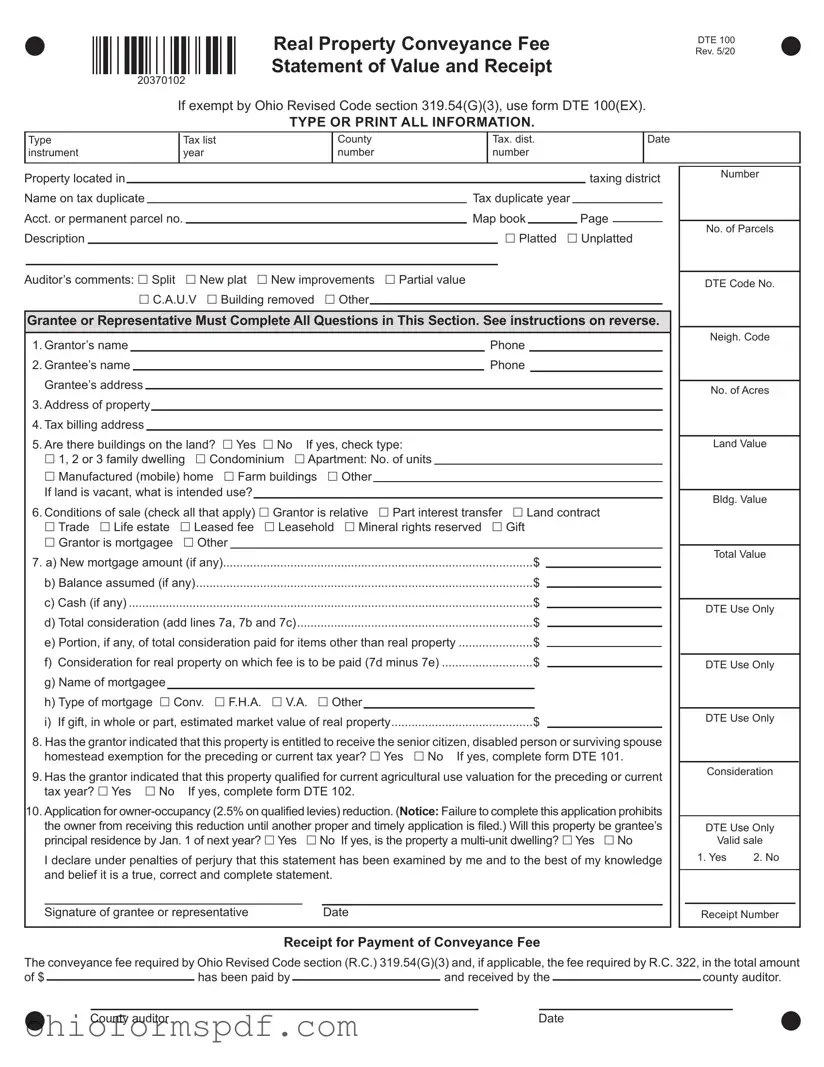

The DTE 100 Ohio form, officially known as the Real Property Conveyance Fee Statement of Value and Receipt, serves as a critical document in the real estate transaction process within Ohio. Revised in May 2020, this form is meticulously designed to facilitate the accurate reporting of a property's value at the time of its conveyance, ensuring the correct calculation and payment of the conveyance fee as mandated by Ohio Revised Code section 319.54(G)(3). It necessitates thorough completion by the grantee or their representative, detailing essential information such as the grantor and grantee's names, property address, conditions of sale, and monetary considerations involved in the transaction. Special conditions affecting the sale, alongside the type and value of the property, are comprehensively covered to determine the applicable fees. Furthermore, the form plays a pivotal role in maintaining uniformity in property tax assessments across the state by providing the county auditor with accurate data. Additionally, it incorporates provisions for exemptions and reductions like the senior citizen, disabled person or surviving spouse homestead exemption, and the current agricultural use valuation, thereby highlighting its significance in the wider fiscal and regulatory framework governing real estate conveyances in Ohio.

Real Property Conveyance Fee Statement of Value and Receipt

DTE 100 Rev. 5/20

20370102

If exempt by Ohio Revised Code section 319.54(G)(3), use form DTE 100(EX).

TYPE OR PRINT ALL INFORMATION.

Type |

Tax list |

County |

Tax. dist. |

Date |

instrument |

year |

number |

number |

|

|

|

|

|

|

Property located in |

|

|

|

|

|

|

|

|

|

taxing district |

||

Name on tax duplicate |

|

|

Tax duplicate year |

|

|

|

||||||

Acct. or permanent parcel no. |

|

Map book |

|

|

|

Page |

|

|||||

Description |

|

|

Platted |

Unplatted |

||||||||

Auditor’s comments: Split New plat New improvements Partial value

C.A.U.V Building removed Other

Grantee or Representative Must Complete All Questions in This Section. See instructions on reverse.

1. Grantor’s name |

|

|

|

Phone |

|

||||

2. Grantee’s name |

|

|

|

|

|

|

Phone |

||

Grantee’s address |

|

|

|

|

|

|

|

||

3. Address of property |

|

|

|

|

|

||||

4. Tax billing address |

|

|

|

|

|

||||

5. Are there buildings on the land? Yes No |

If yes, check type: |

||||||||

1, 2 or 3 family dwelling Condominium |

Apartment: No. of units |

|

|

||||||

Manufactured (mobile) home Farm buildings Other If land is vacant, what is intended use?

6. Conditions of sale (check all that apply) Grantor is relative Part interest transfer Land contract Trade Life estate Leased fee Leasehold Mineral rights reserved Gift

Grantor is mortgagee Other

7. a) New mortgage amount (if any) |

$ |

|||

b) Balance assumed (if any) |

$ |

|||

c) Cash (if any) |

$ |

|||

d) Total consideration (add lines 7a, 7b and 7c) |

$ |

|||

e) Portion, if any, of total consideration paid for items other than real property |

$ |

|||

f) Consideration for real property on which fee is to be paid (7d minus 7e) |

$ |

|||

g) Name of mortgagee |

|

|

|

|

h) Type of mortgage Conv. F.H.A. V.A. Other |

|

|

|

|

i) If gift, in whole or part, estimated market value of real property..........................................$

8. Has the grantor indicated that this property is entitled to receive the senior citizen, disabled person or surviving spouse homestead exemption for the preceding or current tax year? Yes No If yes, complete form DTE 101.

9. Has the grantor indicated that this property qualified for current agricultural use valuation for the preceding or current

tax year? Yes No If yes, complete form DTE 102.

10.Application for

principal residence by Jan. 1 of next year? Yes No If yes, is the property a

I declare under penalties of perjury that this statement has been examined by me and to the best of my knowledge and belief it is a true, correct and complete statement.

Number

No. of Parcels

DTE Code No.

Neigh. Code

No. of Acres

Land Value

Bldg. Value

Total Value

DTE Use Only

DTE Use Only

DTE Use Only

Consideration

DTE Use Only

Valid sale

1. Yes |

2. No |

Signature of grantee or representative |

Date |

Receipt Number

Receipt for Payment of Conveyance Fee

The conveyance fee required by Ohio Revised Code section (R.C.) 319.54(G)(3) and, if applicable, the fee required by R.C. 322, in the total amount

of $ |

|

|

has been paid by |

|

and received by the |

|

county auditor. |

|||

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

County auditor |

|

|

Date |

|

|

||||

DTE 100

Instructions to Grantee or Representative for Completing Rev. 5/20

Real Property Conveyance Fee Statement of Value

Complete lines 1 through 10 in box.

Page 2

WARNING: All questions must be completed to the best of your knowledge to comply with Ohio Revised Code (R.C.) section 319.202.

Persons willfully failing to comply or falsifying information are guilty of a misdemeanor of the first degree (R.C. section 319.99(B)). It is important that the information on this form be accurate as it will be used to determine whether all real property, including this property, is uniformly assessed for real property tax purposes.

Note: The county auditor has discretionary power under R.C. section 319.202(A) to request additional information in any form of documentation deemed necessary to verify the accuracy of the information provided by the grantee on the front of the form.

Line 1 List grantor’s name as shown in the deed or other instrument conveying this real property.

Line 2 List grantee’s name as shown in the deed or other instrument conveying this real property and the grantee’s mailing address.

Line 3 List address of property conveyed by street number and name.

Line 4 List complete name and address to which tax bills are to be sent. CAUTION: Each property owner is responsible for paying the property taxes on time even if no tax bill is received.

Line 5 If there are no buildings on the land conveyed, check “no.” If there are buildings, check “yes” and the appropriate box that describes the type of buildings. If other, describe briefly the type of buildings, such as “office building.”

Line 6 Show any special condition of sale that would affect the consideration. If any of the special conditions noted are involved, check the appropriate box. Briefly describe other conditions in the space provided.

Line 7 a) Enter amount of new mortgage on this property (if any).

b)Enter amount of the balance assumed on an existing mortgage (if any).

c)Enter cash paid for this property (if any).

d)Add lines 7a, 7b and 7c.

e)If any portion of the consideration reported on line 7d was paid for items other than real property, enter the portion of the consideration paid for those items.

f)Deduct line 7e from line 7d and enter the difference on this line.

g)List mortgagee or mortgagees (the party who advances the funds for a mortgage loan).

h)Check type of mortgage.

i)In the case of a gift, in whole or part, enter the estimated price that the real estate would bring in the open market.

Line 8 If the grantor has indicated that the property to be conveyed will receive the senior citizen, disabled person or surviving spouse homestead exemption for a proceeding or current tax year under R.C. section 323.152(A), grantor must complete DTE 101 or submit a statement that complies with the provisions of R.C. section 319.202(A)(2), and the grantee must submit such form to the county auditor along with this statement.

Line 9 If the grantor has indicated that the property to be conveyed qualified for current agricultural use valuation for the preceding or

current tax year under R.C. section 5713.30, the grantor must complete DTE 102 or a statement that complies with R.C. section 319.202(B)(2), and the grantee must submit such form to the county auditor along with this statement.

Line 10 Complete line 10 (application for

as your principal place of residence (domicile) on Jan. 1 of that year. A homeowner and spouse may receive this reduction on

only one home in Ohio. Failure to complete this application prohibits the owner from receiving this reduction until another proper and timely application is filed.

The real property conveyance fee is payable on the amount of money reported on either item 7f or 7i.

| Fact Name | Description |

|---|---|

| Form Title | Real Property Conveyance Fee Statement of Value and Receipt (DTE 100) |

| Revision Date | May 2020 (Rev. 5/20) |

| Governing Law | Ohio Revised Code section 319.54(G)(3) |

| Exemption Form | If exempt by Ohio Revised Code section 319.54(G)(3), use form DTE 100(EX). |

| Main Purpose | To declare the value of real property for the purpose of calculating conveyance fees during property transfer. |

| Completion Requirement | All sections must be completed to comply with Ohio Revised Code (R.C.) section 319.202. |

After you receive the DTE 100 Ohio form, it's crucial to fill it out carefully and completely. This document is necessary for the transaction involving real property. The details you provide will be used to ensure that property taxes are assessed accurately and fairly for all properties. The information you submit must be accurate, as failure to comply or providing false information is taken seriously and is punishable by law. Once the form is completed, it will allow the necessary processing of fees related to the property transaction. Below are step-by-step instructions to assist you in filling out the form accurately.

Once the form is filled out and submitted, the county auditor will process the conveyance fee based on the valuation provided. This step is crucial to ensuring that the property's sale or transfer is recorded properly and that taxation is applied accordingly. Ensure all information is correct and keep a copy of the completed form for your records.

What is the DTE 100 form used for in Ohio?

The DTE 100 form, also known as the Real Property Conveyance Fee Statement of Value and Receipt, is used in Ohio to document the transfer of title in real estate transactions. It ensures that all relevant information about the sale or transfer is accurately reported to the county auditor. This form plays a crucial role in the calculation of conveyance fees, which are required by Ohio Revised Code section 319.54(G)(3), and helps in the accurate assessment of real property taxes.

Who needs to complete the DTE 100 form?

The grantee, or the recipient of the property, is responsible for completing the DTE 100 form. All questions in the specified section of the form must be filled out thoroughly to comply with Ohio Revised Code section 319.202. This includes providing details about the grantor and grantee, the property address, conditions of the sale, and financial information related to the transaction. A signature from the grantee or their representative is required to validate the information provided.

Are there any conditions where the DTE 100 form is not required?

Yes, there are certain exemptions specified under Ohio Revised Code section 319.54(G)(3) where the DTE 100 form is not required. One such instance is when the real property conveyance falls under specific exemptions that qualify it for non-taxable status. In these situations, an alternative form, the DTE 100(EX), is used instead. The DTE 100(EX) form is applicable in cases where the transfer is exempt from conveyance fees according to the Ohio Revised Code.

What documents need to be submitted along with the DTE 100 form?

Alongside the DTE 100 form, additional documents or forms may be required depending on the circumstances of the property transfer. For instance, if the grantor has indicated that the property is entitled to the senior citizen, disabled person, or surviving spouse homestead exemption, form DTE 101 must be completed. Similarly, if the property qualified for the current agricultural use valuation, form DTE 102 is required. These forms help in establishing the eligibility for specific tax exemptions or reductions.

How is the conveyance fee calculated on the DTE 100 form?

The conveyance fee on the DTE 100 form is calculated based on the total consideration paid for the real property, as reported in section 7 of the form. The fee payable is on the amount after deducting any portion of the consideration paid for items other than real property (e.g., personal property included in the sale). The exact fee rate is determined by county regulations, in accordance with Ohio Revised Code section 319.54(G)(3). The calculation involves adding any new mortgage amount, the balance assumed, and any cash payment, then adjusting for non-real property items to arrive at the taxable consideration for the real property.

Filling out the DTE 100 Ohio form, the Real Property Conveyance Fee Statement of Value and Receipt, is a critical step in the process of property conveyance. It requires careful attention to detail. Unfortunately, mistakes can occur, which might lead to delays or complications in the property transfer process. Here are seven common errors made when completing the form:

Attending to these details can make the process smoother and help ensure all legal and tax implications are appropriately managed. It's always a good idea to review the form carefully and consult with a professional if you have any questions or concerns.

When engaging in property transactions in Ohio, the DTE 100 Ohio form, known formally as the Real Property Conveyance Fee Statement of Value and Receipt, plays a crucial role in documenting the exchange. This form not only facilitates the proper assessment of property values for tax purposes but also ensures compliance with legal standards. Alongside the DTE 100, there are other documents and forms that often accompany it, each serving a specific purpose in the property conveyance process. Understanding these documents can significantly streamline the process, providing clarity and efficiency to all parties involved.

Each document associated with the DTE 100 Ohio form serves a unique purpose in the property conveyance process, addressing different aspects of property and ownership that can impact tax obligations and legal rights. By ensuring that all relevant forms are correctly completed and submitted, property conveyances can proceed smoothly, providing security and peace of mind for both grantors and grantees. It's a collaborative effort that safeguards the interests of all parties and maintains the integrity of the real estate market in Ohio.

The DTE 100 form, playing a crucial role in the conveyance of real property within Ohio, shares similarities with various other documents due to its focus on property transactions and tax considerations. One such document is the HUD-1 Settlement Statement, a standard form used across the United States in real estate transactions. Both the DTE 100 and HUD-1 detail the financial aspects of property transfers, itemizing fees, taxes, and other charges for both the buyer and the seller. However, while the DTE 100 is specific to the state of Ohio and primarily concerned with the conveyance fee calculation and tax-related declarations, the HUD-1 has a broader scope, encompassing a complete closing statement for real estate transactions.

Another comparable document is the DTE 100(EX), which is a variant of the DTE 100 form specifically designed for transactions that are exempt from conveyance fees under Ohio law. Both documents require similar information about the property and parties involved, but the DTE 100(EX) highlights transactions that do not fall under the typical conveyance fee requirements due to specific exemptions outlined in the Ohio Revised Code. These exemptions might include transfers between certain family members or transfers to or from governmental entities, emphasizing the flexibility within property transaction processes to accommodate various legal and familial situations.

The Grant Deed is also akin to the DTE 100 form in its function of facilitating property transfers, but it approaches from a different legal standpoint. While the DTE 100 is focused on the financial and tax implications of a real estate transaction, a Grant Deed is a legal document that actually conveys the property from the grantor to the grantee. It guarantees that the property has not been sold to someone else and is free of encumbrances, apart from those the seller has disclosed. This shows how transfer-related documents can serve complementary roles in solidifying the legality and financial clarity of property transactions.

Lastly, the Mortgage Deed, another integral document in property transactions, shares similarities with the DTE 100 by involving property descriptions and financial details. It specifically secures the loan on the real property as collateral for the borrowing involved in the transaction. While the DTE 100 captures the transaction’s financial overview and tax implications, the Mortgage Deed delves into the specifics of the loan and the lender’s interest in the property. This specificity underscores the interconnected roles various documents play in ensuring comprehensive legal coverage for all aspects of property conveyance.

When completing the DTE 100 Ohio form, which is the Real Property Conveyance Fee Statement of Value and Receipt, it's crucial to pay attention to both what should and shouldn't be done to ensure compliance and accuracy. The form plays a pivotal role in real estate transactions within Ohio, guiding the conveyance fee process. Here are some essential dos and don'ts to consider:

Do:

Don't:

Understanding the DTE 100 Ohio form, titled "Real Property Conveyance Fee Statement of Value and Receipt," is crucial for parties involved in real estate transactions in Ohio. However, there are several misconceptions about the form and its requirements. Here, several of these misunderstandings are clarified to offer better insight into the form's function and importance.

Misconception 1: The DTE 100 form is only for the sale of properties with buildings.

This is incorrect. The form is used for the conveyance of real property, regardless of whether there are buildings on the land. The form specifically asks if there are buildings on the land and what type, indicating its applicability to both vacant and developed land.

Misconception 2: The form is not required if the conveyance is exempt from conveyance fees.

Even if a conveyance is exempt from fees under Ohio Revised Code section 319.54(G)(3), a version of this form, the DTE 100(EX), must still be completed. This underscores that compliance with documentation requirements is necessary even when fees are not applicable.

Misconception 3: All conveyances must disclose the purchase price in detail on the form.

While the form requires detailed information about the consideration for the property, including new mortgages, assumed mortgages, and cash paid, it also requires reporting the portion of consideration paid for items other than real property. This allows for a nuanced understanding of the transaction's financial aspects, not just a blanket disclosure of the purchase price.

Misconception 4: The form is only necessary for officially completed sales.

The form is required for the conveyance of real property, which includes not only completed sales but also land contracts, trades, life estates, and other forms of property transfer. It plays a crucial role in documenting agreements that may not result in immediate changes in possession or ownership on paper.

Misconception 5: Individuals can bypass the form if they provide all the necessary information directly to the county auditor.

The Ohio Revised Code requires that this specific form (or its exempt counterpart, DTE 100(EX)) be completed and submitted. The county auditor may request additional documentation, but this does not eliminate the need for the form itself as the primary document for conveyance information.

Misconception 6: Completing the DTE 100 form is the responsibility of the conveyance professional or attorney only.

While professionals often assist in completing the form, the responsibility ultimately lies with the grantee, or buyer, of the property. The grantee or their representative must ensure that all questions are answered accurately, as indicated by the signature requirement at the end of the form.

By addressing these misconceptions, individuals involved in the conveyance of real property in Ohio can better understand their obligations and the importance of the DTE 100 form. Proper completion and submission of this form are vital to the legal and efficient transfer of property rights.

When dealing with the DTE 100 Ohio form, it's important to keep several key points in mind to ensure accurate and compliant completion. Here are nine takeaways to guide you through the process:

Remember, this information will be used for tax purposes and to ensure the property is assessed uniformly with others in the area. Completing this form accurately is crucial to comply with Ohio Revised Code and to avoid potential misdemeanors for falsifying information.

Ohio Tax Forms - Businesses must complete the IT-942 form to provide a comprehensive summary of their tax withholding activities for the year.

How Do I Find Out How Much I Owe the Ohio Attorney General - Focused on reducing the turnaround time for obtaining critical debt information and facilitating timely debt resolution.