Blank Ohio 3 Q Template

Blank Ohio 3 Q Template

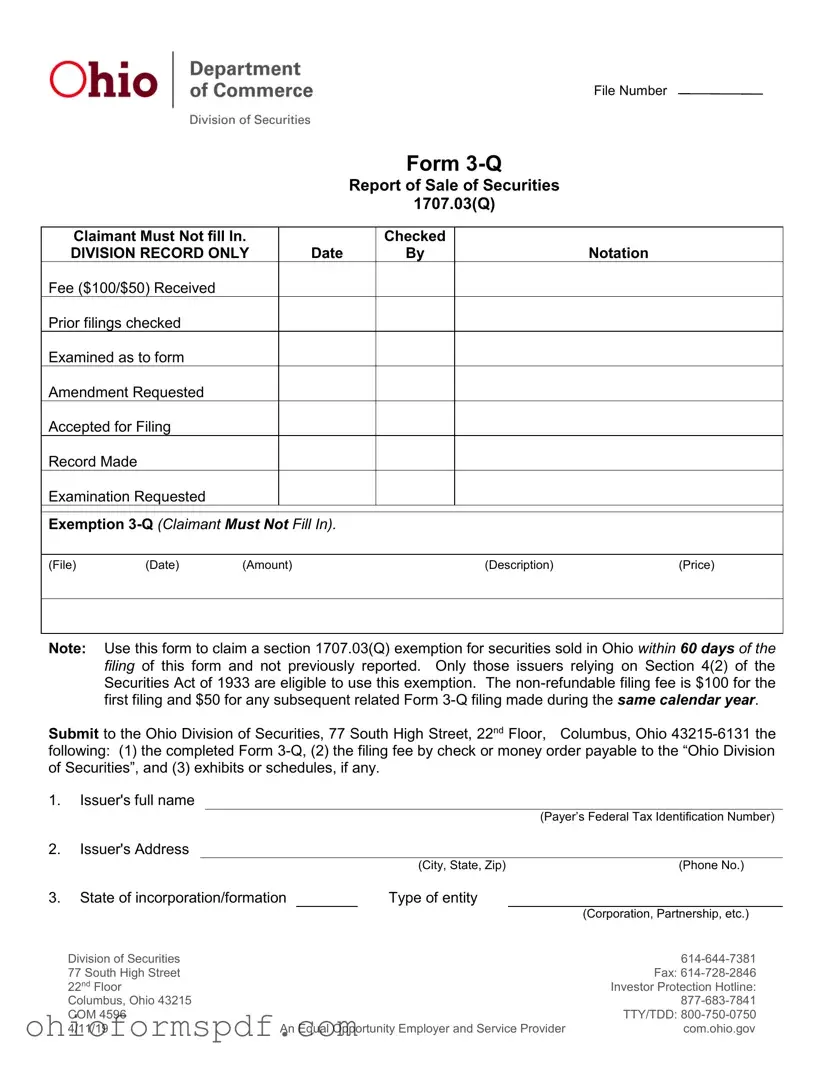

In the complex landscape of securities sales within Ohio, the Form 3-Q emerges as a crucial document for issuers aiming to navigate the intricacies of regulatory compliance with precision. Sited at 77 South High Street in Columbus, the Ohio Division of Securities mandates this form for reporting the sale of securities that claim an exemption under section 1707.03(Q), a niche carved out specifically for offerings that have not been previously reported and are sold within 60 days of this form's filing. Targeted at issuers who hinge their exemption on Section 4(2) of the Securities Act of 1933, Form 3-Q outlines a strict protocol encompassing the submission of detailed information about the securities sold, the involved parties, and the transaction specifics, coupled with a non-negotiable filing fee. Furthermore, it underscores the prohibition against utilizing certain Rules as a basis for exemption and necessitates an exacting disclosure regarding commissions, the usage of offering circulars, and the continuation status of the offering. By adhering to these stipulations, including the necessitated filings for out-of-state or unincorporated issuers through Form 11 or Form U-2, and the recommendation of certified mailing for guaranteed receipt, the meticulously designed Form 3-Q not only serves as a testament to Ohio's commitment to maintaining a transparent, regulated securities marketplace but also as a guidepost for issuers on achieving compliance while fostering investor confidence.

File Number

|

|

|

|

|

|

Form |

|

|

|

|

|

|

|

Report of Sale of Securities |

|

||

|

|

|

|

|

|

1707.03(Q) |

|

|

|

|

|

|

|

|

|

||

Claimant Must Not fill In. |

|

|

|

Checked |

|

|

||

DIVISION RECORD ONLY |

|

Date |

|

By |

|

Notation |

||

Fee ($100/$50) Received |

|

|

|

|

|

|

|

|

Prior filings checked |

|

|

|

|

|

|

|

|

Examined as to form |

|

|

|

|

|

|

|

|

Amendment Requested |

|

|

|

|

|

|

|

|

Accepted for Filing |

|

|

|

|

|

|

|

|

Record Made |

|

|

|

|

|

|

|

|

Examination Requested |

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

Exemption |

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

(File) |

(Date) |

(Amount) |

|

|

|

(Description) |

(Price) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Note: Use this form to claim a section 1707.03(Q) exemption for securities sold in Ohio within 60 days of the filing of this form and not previously reported. Only those issuers relying on Section 4(2) of the Securities Act of 1933 are eligible to use this exemption. The

Submit to the Ohio Division of Securities, 77 South High Street, 22nd Floor, Columbus, Ohio

1.Issuer's full name

(Payer’s Federal Tax Identification Number)

2.Issuer's Address

(City, State, Zip)(Phone No.)

3. State of incorporation/formation |

|

Type of entity |

|

||

|

|

|

|

|

(Corporation, Partnership, etc.) |

Division of Securities |

|

|

|

|

|

77 South High Street |

|

|

|

|

Fax: |

22nd Floor |

|

|

|

|

Investor Protection Hotline: |

Columbus, Ohio 43215 |

|

|

|

|

|

COM 4596 |

|

|

|

|

TTY/TDD: |

4/11/19 |

An Equal Opportunity Employer and Service Provider |

com.ohio.gov |

|||

Ohio Department of Commerce |

FORM |

4.Correspondence regarding this report should be sent to:

(Name) |

(Street) |

(City, State, Zip Code) |

(Phone No.) |

5.A section 1707.03(Q) claim of exemption is being made for the following securities sold in Ohio within 60 days of the filing of this form and not previously reported (use additional sheet, if necessary):

Type of |

|

Date of |

|

Number of |

|

Price |

|

Number of |

Securities Sold |

|

Sale |

|

Units Sold |

|

per Unit |

|

Purchasers |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Note: |

O.A.C. rule |

|

agreement or its equivalent, signed by the purchaser, is received by the issuer or the dealer, or the purchaser |

|

transfers or loses control of the purchase funds, whichever is earlier; or (b) the first date of disbursement of |

|

any proceeds of the sale of the securities which have been deposited directly into an escrow account. |

6.Confirm that the basis in law for this claim of exemption from Section 5 of the Securities Act of 1933 is pursuant to Section 4(2) of that Act. Note that Rules 504, 505 and 506 cannot be used as a basis for claiming the exemption pursuant to Section 1707.03(Q).

7.List the total number of persons who have purchased this offering to date, both in and outside of Ohio, including persons claimed on all previous Form

8.(a) List any commissions, discounts, or other remuneration paid or to be paid or given to any person,

directly or indirectly, for sales in Ohio of the securities claimed on the Form

Name and address of person |

|

Amount of |

|

Percentage of |

receiving commission, etc. |

|

commission, etc. |

|

the Initial Offering Price |

|

|

|

|

|

|

|

|

|

|

(b)Were above commissions, discounts, or other remuneration paid or given only to dealers or

salesmen licensed under Chapter 1707 of the Revised Code? |

YES |

NO |

9.Was an offering circular used in connection with the sales reported on this Form

YES |

NO |

|

If yes, |

Copy attached or |

Previously submitted |

Ohio Department of Commerce |

FORM |

|

10. Has this offering been terminated? YES |

NO |

|

If yes, date of termination |

|

|

11.Incorporated issuers not domiciled in this state or unincorporated issuers having a situs of its principal place of business outside this state must file a Form 11 or Form

SIGNATURE

The undersigned represents that the foregoing information is true as of the date hereof and agrees that this report shall be considered a written statement used for the purpose of selling securities in Ohio within the meaning of Section 1707.44(B) of the Ohio Revised Code. The individual signing this report on behalf of the issuer further represents that he/she is duly authorized by the issuer to execute and file this report.

Issuer or Dealer

|

|

(Full Name) |

By |

|

|

|

(Signature) |

(Date) |

|

|

|

|

(Name) |

(Official Capacity) |

The Division suggests Form

COM 4596 |

Updated 4/11/19 |

| Fact Name | Detail |

|---|---|

| Governing Law | The form is governed by Ohio Revised Code Section 1707.03(Q) and is also subject to the provisions of the Securities Act of 1933, specifically Section 4(2). |

| Primary Purpose | This form is used to report the sale of securities in Ohio that are claimed under the exemption provided by Section 1707.03(Q) and were sold within 60 days of filing this form without prior reporting. |

| Filing Fee | The filing fee for the initial report is $100, with any subsequent related filings during the same calendar year requiring a fee of $50. |

| Eligibility Criteria | Only issuers relying on Section 4(2) of the Securities Act of 1933 are eligible to claim the exemption provided by Section 1707.03(Q). |

| Submission Requirements | Issuers must submit a completed Form 3-Q, the corresponding filing fee, and any relevant exhibits or schedules to the Ohio Division of Securities. |

| Address for Submission | Submissions should be sent to the Ohio Division of Securities located at 77 South High Street, Columbus, Ohio 43215-6131. |

| Exemption Claim Requirements | The claim for exemption must detail the type of securities sold, the date of sale, number of units sold, price per unit, and the number of purchasers. The basis for the lawful claim of exemption needs to reference Section 4(2) of the Securities Act of 1933, specifically noting that Rules 504, 505, and 506 are not viable for this exemption claim. |

Filling out the Ohio Form 3-Q is a straightforward process if done with careful attention to detail. This form is critical for issuers who wish to claim a Section 1707.03(Q) exemption for securities sold in Ohio. It's important to gather all necessary information beforehand, including details about the securities sold and any remunerations paid. A precise compilation of this information facilitates compliance with Ohio's legal requirements and helps ensure the exemption is granted. Additionally, timely and accurate filling of this form prevents potential legal complications and fosters trust among investors. Below are the steps to accurately complete and submit the Ohio Form 3-Q.

Once completed, gather the signed Form 3-Q, the appropriate filing fee by check or money order payable to the “Ohio Division of Securities,” and any required exhibits or schedules. It's recommended to send these documents via certified mail to the Ohio Division of Securities at 77 South High Street, Columbus, Ohio 43215-6131, for verification of receipt. Additionally, including a self-addressed stamped envelope ensures the return of a filed copy for your records.

What is the purpose of the Ohio 3-Q form?

The Ohio 3-Q form is designed for issuers to claim a section 1707.03(Q) exemption for securities sold in Ohio. This exemption applies to sales made within 60 days of the form's filing and for securities not previously reported. It is exclusively available to issuers relying on Section 4(2) of the Securities Act of 1933.

Who needs to fill out the Ohio 3-Q form?

Issuers of securities intending to claim an exemption under section 1707.03(Q) for sales made in Ohio must complete the form. This is pertinent to those who have conducted sales that require reporting and have not been previously filed, provided they qualify under Section 4(2) of the Securities Act of 1933.

What is the filing fee associated with the Ohio 3-Q form?

A non-refundable filing fee is required when submitting the Ohio 3-Q form. The initial filing attracts a $100 fee, with any subsequent related filings made during the same calendar year costing $50 each.

Where do I send the completed Ohio 3-Q form and the associated fee?

The completed form along with the necessary filing fee, paid via check or money order to the "Ohio Division of Securities", should be submitted to the Ohio Division of Securities, located at 77 South High Street, 22nd Floor, Columbus, Ohio 43215-6131.

Can Rules 504, 505, and 506 be used as a basis for claiming the exemption under Section 1707.03(Q)?

No, the exemption under Section 1707.03(Q) cannot be claimed based on Rules 504, 505, and 506. The exemption must be claimed pursuant to Section 4(2) of the Securities Act of 1933 only.

What should be included if commissions were paid for the sales of securities?

If any commissions, discounts, or other remuneration were paid or are to be paid for sales of securities in Ohio, these should be detailed on the form. This includes the name and address of the recipient, the amount, and the percentage of the initial offering price. If none were paid, the issuer should state "None".

Is there a requirement for companies not domiciled in Ohio?

Yes, incorporated issuers not domiciled in Ohio or unincorporated issuers whose principal place of business is outside of Ohio must file a Form 11 or Form U-2, as referenced in section 1707.11 of the Revised Code.

Filling out the Ohio 3-Q form can seem straightforward, but there are common mistakes that people often make. Paying attention to these missteps can ensure that your submission is accurate and avoids unnecessary delays.

These mistakes can impede the processing of your form, potentially leading to delays or the need for amendments. Taking the time to review and ensure all information is correct and complete before submission can save time and help in the seamless processing of your exemption claim.

When preparing and submitting the Ohio 3-Q form, it's crucial to have a comprehensive understanding of the associated paperwork that may be required or beneficial throughout the process. This list highlights additional forms and documents frequently used alongside the Ohio 3-Q form to ensure a thorough and compliant submission to the Ohio Division of Securities.

Understanding and preparing the necessary documentation is critical for a successful securities offering in Ohio. Each document serves a distinct purpose, ensuring that the offering is transparent, compliant, and attractive to potential investors. The Ohio 3-Q form and its accompanying documents facilitate a smooth process for issuers looking to navigate the complexities of securities regulations in the state.

The Form D Notice of Exempt Offering of Securities is one document that shares similarities with the Ohio 3-Q form. Both forms are used in the context of securities exemptions, although they cater to different jurisdictions and laws. The Form D is filed with the U.S. Securities and Exchange Commission (SEC) and is utilized by companies to notify the SEC of an offering of securities that is exempt from the full registration requirements under the Securities Act of 1933, such as under Regulation D. Similarly, the Ohio 3-Q form is used by entities to claim exemption from registration for securities sold in Ohio, specifically under section 1707.03(Q), serving a similar purpose at the state level by providing notification of and details on exempt securities offerings.

The Form U-1 Uniform Application to Register Securities is another document that parallels the Ohio 3-Q form in intent but differs in specific context and requirements. The form U-1 is part of a coordinated registration process for securities offerings across multiple states, aimed at standardizing the information required from issuers seeking to register their securities for public sale. The Ohio 3-Q, conversely, is utilized specifically within Ohio to claim an exemption for securities that do not undergo the full registration process, highlighting the focus of the U-1 on registration versus the 3-Q's focus on exemption from registration within the realm of state-level securities regulation.

The Form U-2 Uniform Consent to Service of Process is an additional document related to the Ohio 3-Q, in that it often accompanies securities filings to authorize service of legal process on a designated entity in each state where a security is offered. While the focus of the Form U-2 is on assuring that issuers can be legally reached in any jurisdiction where they offer securities, it complements the Ohio 3-Q by fulfilling one of the legal requirements for companies that seek to utilize exemptions from registration when offering securities. This shows how documents catering to logistical and legal formalities accompany those like the 3-Q that substantively address the securities offering exemptions.

Lastly, the Form 11 or Form U-2 mentioned within the Ohio 3-Q document itself is akin to the 3-Q in serving issuers who are not domiciled in Ohio or have their principal place of business elsewhere but are engaging in securities offerings within Ohio. These forms are required for issuers in these circumstances to ensure compliance with Ohio's specific securities regulations, especially in cases where issuers might not otherwise be obligated to engage with Ohio's regulatory framework. In this way, the Form 11 or Form U-2 requirement underscores the function of the 3-Q in regulating interstate securities offerings and ensuring that out-of-state entities comply with Ohio's securities laws, similarly aiming to protect investors and maintain market integrity within the state.

When filling out the Ohio 3-Q form for reporting the sale of securities, it is important to follow specific guidelines to ensure the submission is accepted and processed correctly. Below are ten recommendations on what you should and should not do during this process.

Following these guidelines can help ensure the submission process is smooth and that all legal requirements are met for the sale of securities in Ohio. Remember, when in doubt, consulting with a lawyer knowledgeable in securities law in Ohio can provide further guidance and help avoid potential legal issues.

When filing the Ohio 3-Q form, several misconceptions can lead to errors or misunderstandings about the process and its requirements. Here are seven common misconceptions:

Understanding these misconceptions is key to ensuring that the filing process is navigated accurately and in compliance with Ohio's securities regulations. It's always recommended to consult with a legal professional when dealing with specific aspects of securities law and filing requirements.

Filling out and using the Ohio 3-Q form involves several key steps and rules to follow. Here are some essential takeaways to ensure the process is handled correctly:

Complying with the above guidelines when preparing the Ohio 3-Q form will aid issuers in successfully claiming the section 1707.03(Q) exemption for their securities sales in Ohio.

Ohio Epa 4309 - Applicants must provide evidence of compliance with local and state regulations, including inter-municipal agreements where applicable.

City of Tiffin - Aids in the efficient allocation of municipal resources in Tiffin by collecting necessary funds through local income taxation.