Blank Ohio Cat Cs Template

Blank Ohio Cat Cs Template

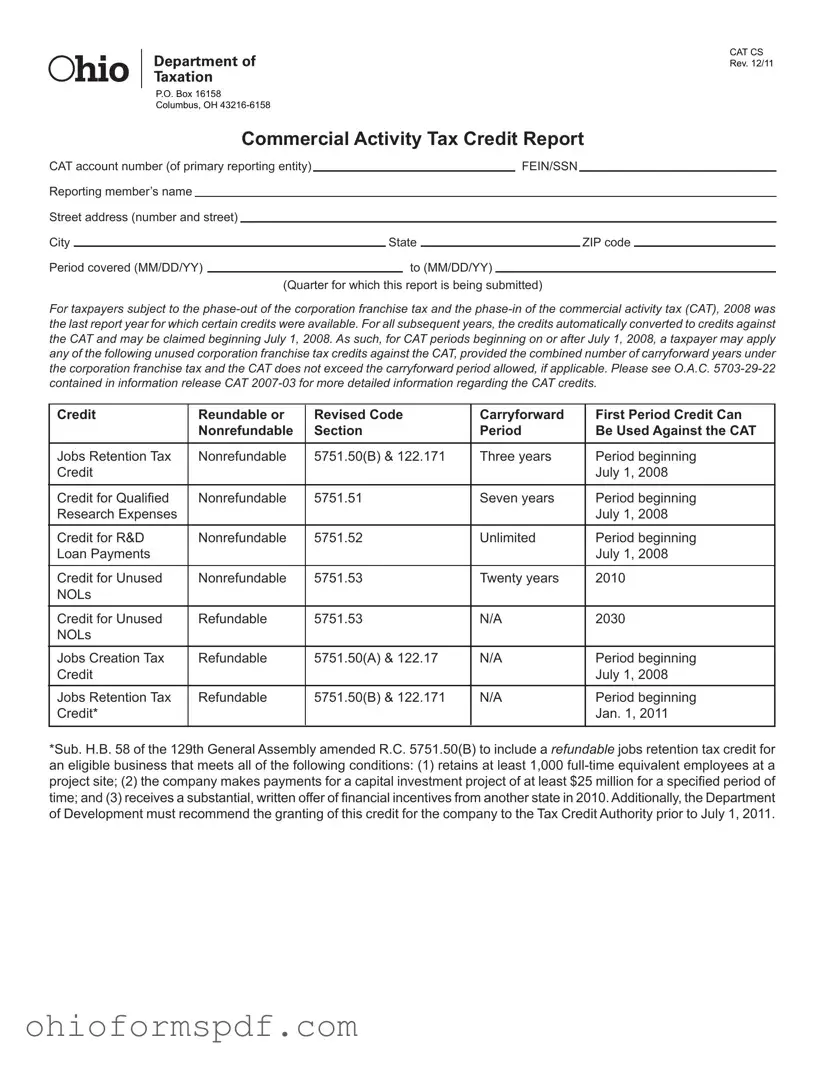

The Ohio Commercial Activity Tax (CAT) Credit Report, an essential document for companies in the transition from the corporation franchise tax to the CAT, signifies a critical shift in Ohio's tax structure that has implications for businesses statewide. Announced with a revision date of December 2011 and addressed from a Columbus, Ohio, P.O. box, this form encompasses vital information for reporting entities including the CAT account number, Federal Employer Identification Number (FEIN) or Social Security Number (SSN), and detailed contact information. Furthermore, it outlines the reporting period and specifies the quarter for which the report is being submitted, illustrating its periodic nature. The phases out of the corporation franchise tax in 2008, and the introduction of the CAT brought significant changes, where certain credits under the former could be applied to the latter from July 1, 2008, onward. This adaptation allowed for the application of unused credits within specified carryforward periods across an array of categories, including jobs retention, qualified research expenses, and research and development (R&D) loan payments, among others. Each credit type is meticulously classified as either refundable or nonrefundable, with explicit reference to the Ohio Revised Code sections that govern their applicability. The form further requires a declaration signed under penalties of perjury, emphasizing the document's legal significance and the accuracy of the information provided, rounding out a comprehensive vehicle for businesses to navigate the complexities of Ohio’s commercial tax obligations.

CAT CS

Rev. 12/11

P.O. Box 16158

Columbus, OH

Commercial Activity Tax Credit Report

CAT account number (of primary reporting entity) |

|

|

|

|

|

FEIN/SSN |

|

|

|

||||

Reporting member’s name |

|

|

|

|

|

|

|

|

|

|

|

|

|

Street address (number and street) |

|

|

|

|

|

|

|

|

|

|

|||

City |

|

|

|

State |

|

|

|

ZIP code |

|

||||

Period covered (MM/DD/YY) |

|

|

|

to (MM/DD/YY) |

|

|

|

|

|||||

|

|

|

|

(Quarter for which this report is being submitted) |

|

|

|

||||||

For taxpayers subject to the

Credit |

Reundable or |

Revised Code |

Carryforward |

First Period Credit Can |

|

Nonrefundable |

Section |

Period |

Be Used Against the CAT |

|

|

|

|

|

Jobs Retention Tax |

Nonrefundable |

5751.50(B) & 122.171 |

Three years |

Period beginning |

Credit |

|

|

|

July 1, 2008 |

|

|

|

|

|

Credit for Qualifi ed |

Nonrefundable |

5751.51 |

Seven years |

Period beginning |

Research Expenses |

|

|

|

July 1, 2008 |

|

|

|

|

|

Credit for R&D |

Nonrefundable |

5751.52 |

Unlimited |

Period beginning |

Loan Payments |

|

|

|

July 1, 2008 |

|

|

|

|

|

Credit for Unused |

Nonrefundable |

5751.53 |

Twenty years |

2010 |

NOLs |

|

|

|

|

|

|

|

|

|

Credit for Unused |

Refundable |

5751.53 |

N/A |

2030 |

NOLs |

|

|

|

|

|

|

|

|

|

Jobs Creation Tax |

Refundable |

5751.50(A) & 122.17 |

N/A |

Period beginning |

Credit |

|

|

|

July 1, 2008 |

|

|

|

|

|

Jobs Retention Tax |

Refundable |

5751.50(B) & 122.171 |

N/A |

Period beginning |

Credit* |

|

|

|

Jan. 1, 2011 |

|

|

|

|

|

*Sub. H.B. 58 of the 129th General Assembly amended R.C. 5751.50(B) to include a refundable jobs retention tax credit for an eligible business that meets all of the following conditions: (1) retains at least 1,000

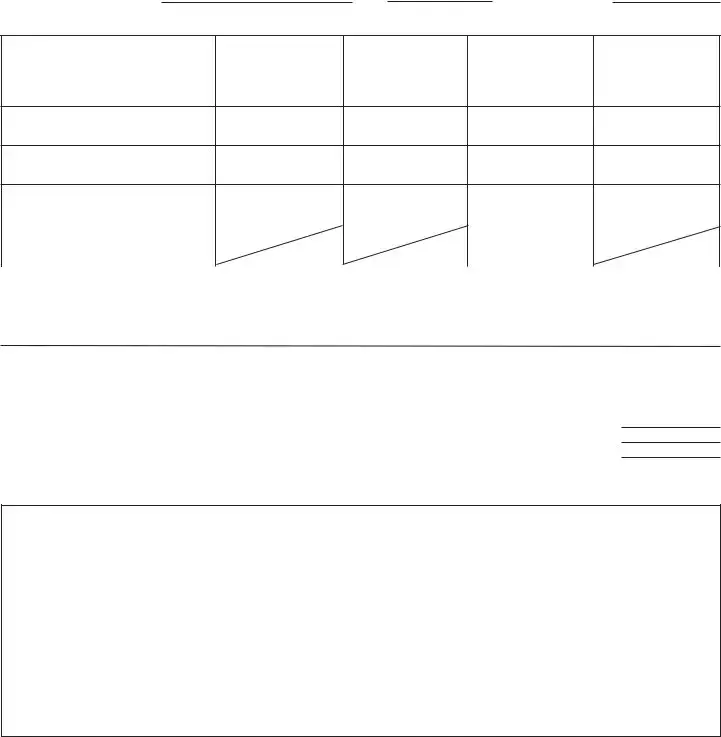

Credit Schedule

(If credits are being claimed by members of a consolidated elected or combined taxpayer group, a separate schedule is required for each entity that is claiming a credit.)

The CAT account number of the entity entitled to the credit may be different than that of the primary reporting entity.

Entity entitled to credit: NameFEINCAT account number

Nonrefundable Credits

A |

B |

C |

D |

|

|

|

|

|

|

Opening Unused |

Credit Earned |

Credits Claimed |

Closing Unused |

|

During Current |

During Current |

|||

Credit Balance |

Credit Balance |

|||

Reporting Period |

Reporting Period |

|||

|

|

1.Jobs retention credit+

2.Qualifi ed research expense credit

3.Research and development loan repayment credit+

4. Total |

|

* |

|

|

|

|

|

|

|

|

|

*Combine with credits being claimed by other entities in group (if any) and carry this forward to line 7 on your CAT return.

+Must attach credit certifi cate received from the Department of Development

Refundable Credits

Must attach credit certifi cate received from the Department of Development

Jobs creation credit |

1. |

Jobs retention credit |

2. |

Total of lines 1 and 2 to be carried forward to line 11 of CAT return |

3. |

Declaration and signature (an offi cer or managing agent of the corporation must sign this declaration)

I declare under penalties of perjury that this report (including any |

use any of its money or property for or in aid of or opposition to |

accompanying schedule or statement) has been examined by |

a political party, a candidate for election or nomination to public |

me and to the best of my knowledge and belief is a true, correct |

office, or a political action committee, legislation campaign fund, |

and complete return and report, and that this corporation has not, |

or organization that supports or opposes any such candidate or |

during the preceding year, except as permitted by Ohio Revised |

in any manner used any of its money for any partisan political |

Code sections 3517.082, 3599.03 and 3599.031, directly or |

purpose whatsoever, or for reimbursement or indemnification of |

indirectly paid, used or offered, consented, or agreed to pay or |

any person for money or property so used. |

|

|

|

|

|

|

||

Date (MM/DD/YY) |

Signature of offi cer or managing agent |

Title |

|||||

|

|||||||

|

|

|

|

|

|

|

|

Contact telephone no. |

|

|

|

|

|||

| Fact Name | Description |

|---|---|

| Form Title and Revision Date | The Ohio CAT CS form, revised as of December 2011. |

| Mailing Address | P.O. Box 16158, Columbus, OH 43216-6158 is the submission address for the form. |

| Primary Purpose | Used for reporting Commercial Activity Tax (CAT) credits. |

| Applicable Tax Credits | Includes credits such as Jobs Retention Tax Credit, Qualified Research Expenses, and R&D Loan Payments. |

| Governing Law(s) | Governed by Ohio Administrative Code 5703-29-22 and information release CAT 2007-03. |

| Carryforward and Use Periods | Specifies periods for which various tax credits may be applied, including those with three years, seven years, twenty years, unlimited, and specific start years for usage against CAT. |

Filling out the Ohio Commercial Activity Tax Credit Report (CAT CS) is a crucial process for businesses looking to claim various tax credits against the Commercial Activity Tax. This form allows entities to report and utilize specific tax credits they've accumulated, such as for jobs retention, research expenses, and more, which could significantly impact the entity's tax obligations. By following the steps below carefully, you can ensure that your claim is appropriately documented and submitted, maximizing the potential benefits for your entity.

After completing the form, double-check all entries for accuracy and completeness. Once satisfied, mail the document to the provided address: P.O. Box 16158, Columbus, OH 43216-6158. Promptly submitting your form ensures that your credits are accounted for in the current reporting period, aiding in accurate and beneficial financial planning for your entity. Remember, keeping copies of all submitted documents is crucial for your records and future reference.

What is the Ohio CAT CS form used for?

The Ohio CAT CS form, officially known as the Commercial Activity Tax Credit Report, is a document utilized by businesses to report and apply various credits against the Commercial Activity Tax (CAT) in Ohio. This form allows entities that were subject to the phase-out of the corporation franchise tax and the introduction of CAT, starting from the year 2008, to apply unused corporation franchise tax credits to the CAT. The form is critical for businesses seeking to leverage these credits to reduce their taxable liability under the CAT regime.

Which credits can be claimed on the Ohio CAT CS form?

Businesses can claim several types of credits on the Ohio CAT CS form, including the Jobs Retention Tax Credit, Credit for Qualified Research Expenses, Credit for R&D Loan Payments, and Credit for Unused Net Operating Losses (NOLs), among others. The credits are primarily nonrefundable, with the exceptions being certain Jobs Creation and Jobs Retention Tax Credits, which are refundable under specific conditions. The form facilitates the application of these credits against the CAT for eligible businesses, adhering to various carryforward periods allowed for each credit type.

What are the reporting requirements for the Ohio CAT CS form?

When completing the Ohio CAT CS form, reporting entities must furnish detailed information including the CAT account number, FEIN/SSN, reporting member’s name, address, and the period covered by the report. The report should specify the unused credits carried over from the corporation franchise tax, earned during the current reporting period, and any used credits. Additionally, separate schedules are required for each entity within a consolidated elected or combined taxpayer group claiming a credit. All claims must be substantiated with a credit certificate received from the Department of Development.

How does a business submit the Ohio CAT CS form and when is it due?

Businesses must submit the Ohio CAT CS form to the specified address in Columbus, Ohio, as outlined on the document. The submission includes a declaration and signature by an officer or managing agent of the corporation, attesting to the accuracy and truthfulness of the information provided under penalties of perjury. The due date for the submission corresponds with the CAT return due dates, varying based on the business's reporting period – monthly, quarterly, or annually. Timely submission is crucial to ensure that eligible credits are properly applied against the CAT liabilities. For specific submission deadlines, businesses should refer to the Ohio Department of Taxation's CAT filing schedule.

Filling out the Ohio CAT CS form, which relates to the Commercial Activity Tax Credit Report, is a critical task for businesses in Ohio aiming to claim their eligible credits. However, mistakes can easily happen if one is not careful. Here are six common errors that people often make when completing this form:

While this might seem daunting, carefully reviewing the form and ensuring all information is correct and complete can significantly streamline the credit claiming process. It's also advisable to consult with a tax professional if there are any uncertainties or complex issues related to your claim.

When preparing to file the Ohio Commercial Activity Tax (CAT) Credit Report, there are several other forms and documents that businesses often find useful to accompany their CAT CS form submission. These additional documents ensure compliance and facilitate a smoother process in managing CAT obligations. Here’s a glimpse of what those documents typically include:

Filing the Ohio CAT CS form, accompanied by the correct forms and documents, is a critical process that businesses need to undertake meticulously. The inclusion of these additional documents not only aids in the accuracy and completeness of the CAT filing but also positions the business more favorably in leveraging potential tax credits and incentives. It's advisable for businesses to maintain orderly records and consult with tax professionals to ensure all their filings are compliant and optimized.

The Ohio Cat Cs form is closely related to the Federal Income Tax Credit form in terms of its structure and purpose. Both forms allow taxpayers, whether individuals or businesses, to report specific tax credits that can reduce their taxable income or tax liability. Just like the Ohio Cat Cs form enables businesses to claim credits for activities such as job retention and research expenses, the Federal Income Tax Credit form includes provisions for credits related to energy efficiency, education, and investment in low-income housing, among others. Each credit outlined is subject to specific qualifying criteria, carryforward periods, and rules about whether the credit is refundable or nonrefundable.

Another document resembling the Ohio Cat Cs form is the State Income Tax Return form found in states that impose an income tax. These state forms also include sections where taxpayers can report and claim various credits against their taxable income. Credits might relate to property taxes paid, education expenses, or investments in renewable energy. The structure of these forms requires detailed information about eligible credits, similar to how the Ohio Cat Cs form requires specific details about credits against the Commercial Activity Tax.

The General Business Credit (Form 3800) used in federal tax filings shares similarities with the Ohio Cat Cs form. It's designed for businesses to aggregate and claim various smaller credits into one larger credit against their income tax. This form encompasses a range of credits, including those for increasing research activities, which is also a feature of the Ohio Cat Cs form. Both forms act as aggregators for different credits and have the underlying aim of encouraging and rewarding certain business behaviors, such as innovation or retaining jobs.

The Research & Development Tax Credit forms, both at the federal and state levels, where applicable, bear resemblance to sections of the Ohio Cat Cs form that pertain to credits for qualified research expenses and R&D loan payments. These forms are dedicated to encouraging businesses to invest in research and development by offering a reduction in tax liability in return. They require detailed reporting of qualifying expenses, mirroring the Ohio form’s structure in the way credits are documented and claimed.

Similarly, the Job Creation Tax Credit forms found in various states are analogous to the Job Creation and Retention sections of the Ohio Cat Cs form. These documents are specifically designed to incentivize businesses to create new jobs or retain existing ones within a state. They outline the eligibility criteria, benefit periods, and sometimes the mechanism for claiming the credit, whether it is refundable or not, closely following the Ohio document's approach to fostering employment growth through tax incentives.

The New Markets Tax Credit (NMTC) application forms, catering to investments in economically disadvantaged areas, share a conceptual parallel with the Ohio Cat Cs form. While the NMTC primarily focuses on encouraging investments that spur economic growth and job creation in low-income communities, it's akin to the Ohio form in its goal of using tax credits as an economic development tool. Applicants must provide detailed information about their investments, similar to how businesses report their qualifying activities for credits on the Ohio form.

The Energy Investment Tax Credit (ITC) forms, which provide credits for investments in energy property, also share similarities with the Ohio Cat Cs form. These forms cater to businesses investing in renewable energy sources, offering them a way to reduce their tax burden in recognition of their contributions to environmental sustainability. The detailed eligibility requirements, claim process, and the distinction between refundable and nonrefundable credits reflect the structure seen in the Ohio Cat Cs form.

Last, the Foreign Tax Credit forms, used by businesses and individuals who have paid or accrued tax to a foreign government, and wish to avoid double taxation, resemble the Ohio Cat Cs form in their purpose to ensure taxpayers are not penalized for operating across borders. Both sets of documents serve to alleviate the tax burden, though in different contexts, by providing a mechanism to claim credits for taxes already paid elsewhere, ensuring that businesses can operate more freely without the hindrance of excessive taxation.

When completing the Ohio Commercial Activity Tax (CAT) Credit Report (CAT CS form), there are specific steps you should follow to ensure accuracy and compliance with state regulations. Below is a list of things to do and not to do when filling out this form:

There are several misconceptions about the Ohio CAT (Commercial Activity Tax) CS form. Understanding these misconceptions is essential for taxpayers and businesses to properly comply with the CAT regulations and benefit from eligible credits. Here are six common misunderstandings:

Addressing these misconceptions ensures that taxpayers accurately complete the CAT CS form and utilize available tax credits effectively.

When dealing with the Ohio CAT (Commercial Activity Tax) CS form, several key aspects need to be considered for accurate completion and submission:

Understanding these points ensures proper reporting of Commercial Activity Tax credits in Ohio, which can significantly impact a company's tax liabilities and compliance status.

Ohio Hea 5802 - Supports research and policy development aimed at reducing lead exposure in Ohio.

Ohio Money - Provides a government-sanctioned method for legitimately reclaiming assets forgotten in Ohio.

Ohio Label Registration - Documentation supporting the application must be accurate and complete to facilitate a smooth review process.