Blank Ohio It 3 Template

Blank Ohio It 3 Template

Staying compliant with tax regulations is crucial for businesses and employers, and this includes properly submitting tax information in Ohio. The Ohio IT 3 form serves as an essential document for transmitting W-2 and 1099-R statements to the Ohio Department of Taxation. With a strict filing deadline of January 31st—or within 60 days after the discontinuation of a business—this form highlights the importance of timely submissions to avoid penalties and ensure compliance. Under the guidelines, electronic submission through the Ohio Business Gateway is strongly advocated for all employers, regardless of the number of W-2 or 1099-R forms they issue, marking a significant move away from paper submissions and CD-ROM options which are no longer accepted. The specifications mandate that those issuing more than 250 statements must utilize the Gateway’s W-2/1099 Upload feature, which generates an IT 3 form automatically from the submitted information, thereby streamlining the process. Conversely, for those issuing fewer statements, electronic filing is encouraged but not mandatory, yet the tax department reserves the right to request electronic submissions for compliance purposes. Additionally, employers are reminded of their duty to retain tax records for four years, emphasizing the importance of record-keeping in managing tax responsibilities. The procedural details, including the elimination of CD submissions and the emphasis on electronic filing, underscore the shift towards more efficient, secure, and environmentally friendly methods of tax reporting.

Ohio IT 3

Transmittal of

Instructions

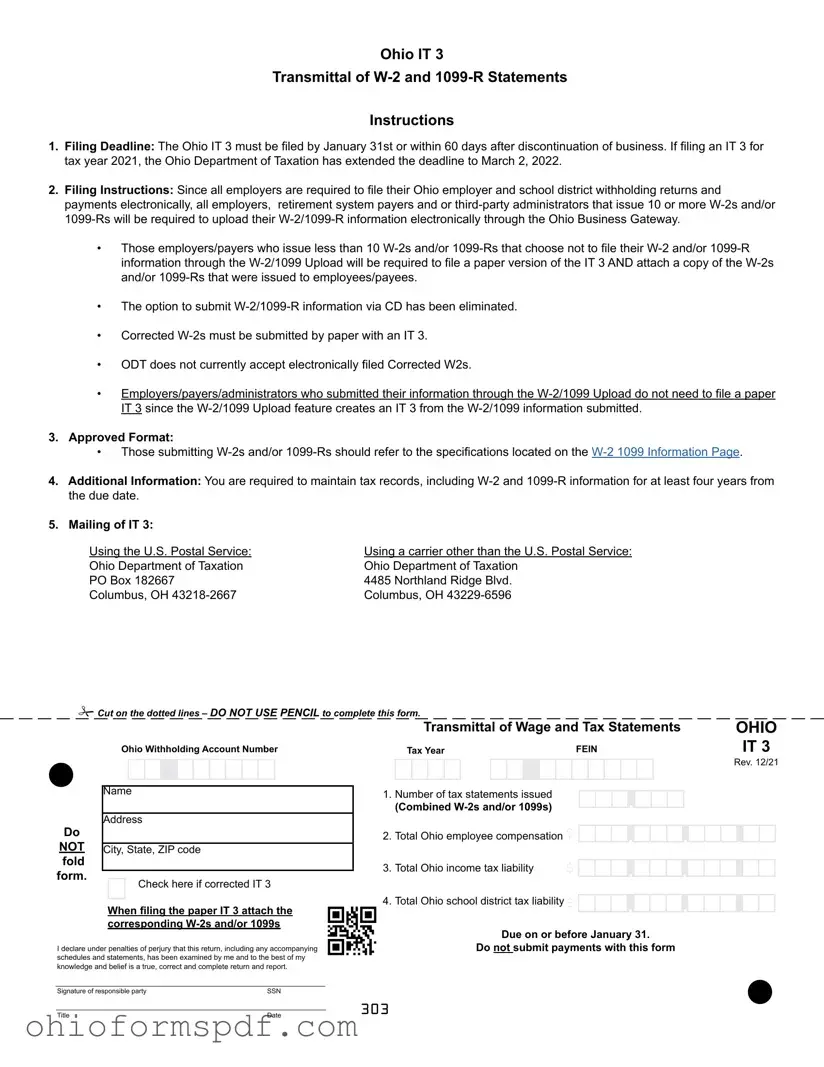

1.Filing Deadline: The Ohio IT 3 must be filed by January 31st or within 60 days after discontinuation of business. If filing an IT 3 for tax year 2021, the Ohio Department of Taxation has extended the deadline to March 2, 2022.

2.Filing Instructions: Since all employers are required to file their Ohio employer and school district withholding returns and payments electronically, all employers, retirement system payers and or

•Those employers/payers who issue less than 10

•The option to submit

•Corrected

•ODT does not currently accept electronically filed Corrected W2s.

•Employers/payers/administrators who submitted their information through the

3.Approved Format:

•Those submitting

4.Additional Information: You are required to maintain tax records, including

5.Mailing of IT 3:

Using the U.S. Postal Service: |

Using a carrier other than the U.S. Postal Service: |

Ohio Department of Taxation |

Ohio Department of Taxation |

PO Box 182667 |

4485 Northland Ridge Blvd. |

Columbus, OH |

Columbus, OH |

Cut on the dotted lines – DO NOT USE PENCIL to complete this form.

|

|

Ohio Withholding Account Number |

||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Name |

|||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Address |

|||||||||||||

Do |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

NOT |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

City, State, ZIP code |

||||||||||||||

fold |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

form. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Check here if corrected IT 3 |

|||||||||||

|

|

|

|

|||||||||||

|

|

|

|

|||||||||||

|

When filing the paper IT 3 attach the |

|||||||||||||

|

corresponding |

|||||||||||||

I declare under penalties of perjury that this return, including any accompanying schedules and statements, has been examined by me and to the best of my knowledge and belief is a true, correct and complete return and report.

Signature of responsible party |

SSN |

|

|

Title |

Date |

|

|

Transmittal of Wage and Tax Statements |

|

|

|

|

OHIO |

|||||||||||||||||||||||||

|

Tax Year |

|

|

FEIN |

|

|

|

|

|

|

IT 3 |

|||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Rev. 12/21 |

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

1. |

Number of tax statements issued |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

, |

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||

|

(Combined |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||

2. |

Total Ohio employee compensation $ |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||

|

|

|

|

|

|

|

, |

|

|

|

|

, |

|

|

|

. |

|

|

|

|||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||

3. |

Total Ohio income tax liability |

$ |

|

|

|

|

|

|

|

, |

|

|

|

|

, |

|

|

. |

|

|

|

|||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||

4. |

Total Ohio school district tax liability$ |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||

|

|

|

|

|

|

|

, |

|

|

|

|

, |

|

|

|

. |

|

|

|

|

||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Due on or before January 31.

Do not submit payments with this form

303

| Fact Number | Fact Detail |

|---|---|

| 1. Submission Deadline | The Ohio IT 3 form must be filed by January 31st or within 60 days after business discontinuation. |

| 2. Electronic Filing Encouragement | All employers are encouraged to submit W-2/1099-R information electronically, regardless of the number of forms issued. |

| 3. CD Submission Option Removal | The option to submit W-2/1099-R information via CD has been eliminated. |

| 4. Electronic Submission Requirement for Bulk | Employers issuing 250 or more W-2s/1099-Rs must submit their information electronically through the Ohio Business Gateway. |

| 5. Guidance for Less than 250 Forms | Employers issuing fewer than 250 W-2s/1099-Rs are encouraged to use the W-2/1099 Upload feature, but can file a paper IT 3 without attachments if choosing not to. |

| 6. Potential Electronic Submission Mandate | The Ohio Department of Taxation may require electronic submission through the W-2/1099 Upload feature for compliance purposes, even if fewer than 250 W-2/1099-R forms are issued. |

| 7. Record Retention | Employers are required to maintain W-2 and 1099 records for at least four years from the due date. |

| 8. Physical Mailing Addresses | There are specific mailing addresses for submissions using the U.S. Postal Service and other carriers. |

| 9. Perjury Declaration | The form includes a declaration under penalty of perjury that the submitted information is accurate. |

| 10. Governing Law | The requirement and procedures for filing the Ohio IT 3 form are governed by Ohio state tax law. |

Filling out the Ohio IT 3 form is an important step for employers in the state of Ohio. This form is a transmittal document for W-2 and 1099-R statements. Understanding how to properly complete and submit this form is crucial to ensuring compliance with Ohio tax regulations. The process requires attention to detail and adherence to the deadlines set by the Ohio Department of Taxation. Below is a simplified guide to help you through the process of completing the Ohio IT 3 form correctly.

After successfully submitting the Ohio IT 3 form, it's essential to keep a copy for your records. This ensures that you have the necessary documentation for future reference or if any questions arise about your submission. Timely and accurate completion of the IT 3 helps maintain compliance with Ohio's taxation requirements, contributing to the smooth operation of your business within the state.

What is the Ohio IT 3 form and who needs to file it?

The Ohio IT 3 form is a transmittal form used primarily for the submission of W-2s and 1099-Rs to the Ohio Department of Taxation. Employers or entities that have issued these documents to their employees or recipients in the state of Ohio are required to file this form. Specifically, it is a summary document that reports total employee compensation, total Ohio income tax liability, and total Ohio school district tax liability based on the W-2 and 1099-R statements issued during the tax year.

What is the deadline for filing the Ohio IT 3 form?

The deadline for filing the Ohio IT 3 form is January 31st of the year following the tax year for which the W-2 and 1099-R statements are being reported. If a business discontinues operations, the form must be filed within 60 days of closure. Meeting this deadline is crucial to avoid non-compliance with state tax regulations.

Are there options for filing the Ohio IT 3 form electronically or by paper?

The preferred and strongly encouraged method for filing Ohio IT 3 forms is electronically through the Ohio Business Gateway (Gateway). Specifically, employers who issue 250 or more W-2s or 1099-Rs must submit their information electronically via the W-2/1099 Upload feature on the Gateway, which automatically generates an IT 3 form from the submitted information. For those issuing fewer than 250 of these forms, electronic submission is encouraged but not mandated. However, the Ohio Department of Taxation may still require electronic submission through the Gateway for compliance purposes, even if fewer than 250 forms are issued. Paper submissions are an option for these smaller issuers, but this method is less favored.

Has the option to submit W-2/1099-R information via CD been maintained?

No, the option to submit W-2/1099-R information via CD has been eliminated. The exclusive method for submitting this information is through the Ohio Business Gateway, ensuring a more streamlined and secure process for the electronic transmission of these documents.

What should be done if one issues less than 250 W-2s or 1099-Rs?

For those issuing less than 250 W-2s or 1099-Rs, electronic submission through the W-2/1099 Upload feature on the Ohio Business Gateway is strongly encouraged but not strictly required. If not using the electronic upload feature, these entities must file a paper IT 3 form directly with the Ohio Department of Taxation. It is important to note, though, that the Department may still mandate the use of the electronic upload feature as part of its compliance enforcement programs, emphasizing the state's push towards electronic reporting.

What records retention policy is recommended for those who file the Ohio IT 3 form?

Entities that file the Ohio IT 3 form are required to retain associated tax records, including W-2 and 1099 information, for a minimum of four years from the due date of the form. This retention policy ensures that necessary documentation is available in case of audits or inquiries from the Ohio Department of Taxation regarding reported figures on the IT 3 form or the accompanying W-2 and 1099-R statements.

Filling out the Ohio IT 3 form can sometimes be trickier than it looks. Avoiding common mistakes can save you time and help ensure that the process goes as smoothly as possible. Here are four common errors people make when completing this form:

Missing the Filing Deadline: One of the most straightforward yet often overlooked aspects is the deadline. The Ohio IT 3 must be filed by January 31st, or within 60 days after discontinuing your business. Failing to meet this deadline can lead to unnecessary delays and complications.

Electronic Submission Oversight: All employers are strongly encouraged to submit their W-2/1099-R information electronically, regardless of the number of forms they issue. It's crucial to note that the option to submit via CD has been removed. Now, the only method for submission is through the Ohio Business Gateway. This requirement is mandatory for those issuing 250 or more W-2s/1099-Rs, and it's a common mistake to overlook this obligation.

Incorrectly Completing Box #1: Whether submitting W-2s or 1099-Rs electronically or on paper, it is essential to correctly complete box #1, indicating the total number of tax statements issued. This box must be filled even if you are not submitting W-2 or 1099-R forms alongside it. A frequent error is leaving this box blank or inaccurately reporting the number of statements, which could raise issues with the Ohio Department of Taxation.

Failing to Maintain Records: After submitting your IT 3 form, it's required that you maintain tax records, including W-2 and 1099 information, for at least four years from the due date. Overlooking or neglecting this requirement can create significant problems if your records are requested by the Ohio Department of Taxation for review.

Avoiding these common mistakes can make a big difference in the filing process. Staying informed and attentive to the specific requirements of the Ohio IT 3 form will facilitate a smoother, more straightforward experience.

When submitting the Ohio IT 3 form, businesses are engaging in a critical compliance step with the state's tax regulations. However, it’s important to be aware that this form often doesn't stand alone. To ensure full compliance and accurate reporting, a number of additional documents may need to be prepared and submitted alongside the Ohio IT 3. These documents support and provide detailed information that complements the data submitted through the IT 3 form.

Together, these documents form a comprehensive reporting suite that supports the data submitted on the Ohio IT 3 form. Employers should ensure these documents are accurately completed and readily available, to not only comply with state tax filing requirements but also to facilitate any inquiries or audits by the Ohio Department of Taxation. Understanding and preparing each of these forms in conjunction with the IT 3 promotes a seamless filing experience and helps uphold the integrity of Ohio's tax system.

The Internal Revenue Service (IRS) W-2 form is notably similar to the Ohio IT 3 form in its fundamental purpose, which is to report wages, tips, and other compensation paid to employees, along with the taxes withheld from these wages. Much like the Ohio IT 3, the W-2 form must be submitted by employers annually. Both forms cater to a similar audience—employers—and serve as critical components in the compliance with tax reporting obligations, facilitating the accurate reporting of employee income and tax withholdings to respective tax authorities.

The IRS 1099-R form, which is used to report distributions from pensions, annuities, retirement or profit-sharing plans, IRAs, insurance contracts, etc., also shares similarities with the Ohio IT 3 form. Both forms are integral to tax reporting and compliance, especially concerning the documentation of income beyond wages. The Ohio IT 3 mentions the 1099-R explicitly, as it encompasses the transmittal of 1099-R statements, indicating a direct relevance and conjunction in their use for reporting purposes.

Form 941, also known by the IRS, is employed by employers to report federal withholdings from employee wages, including social security and Medicare taxes. This form's submission frequency and its role in reporting crucial tax deduction information make it akin to the Ohio IT 3 form. While the IT 3 focusses on state-level income and school district tax liabilities, Form 941 addresses federal tax obligations, highlighting the interconnected nature of tax reporting across different government levels.

The Bureau of Labor Statistics' (BLS) Quarterly Census of Employment and Wages (QCEW) program uses federal and state data to compile a comprehensive report on employment and wage trends across the U.S. Though not a direct form like the Ohio IT 3, the QCEW's data collection process is reminiscent of the IT 3's role in aggregating employment income and tax information, contributing to a broader understanding of labor market dynamics at the state and national levels.

The Ohio Employer's Quarterly Unemployment Tax Return (form JFS 20125) mirrors the Ohio IT 3 in its quarterly reporting requirement, albeit focusing on unemployment tax contributions rather than wage and tax statements. Both forms are pivotal for employers in Ohio, ensuring compliance with state tax laws and supporting the administration of employment-related tax programs.

The Ohio SD 101 form serves as the School District Income Tax Withholding Payment Voucher, which is similar to the Ohio IT 3 form in its focus on school district tax considerations. While the IT 3 includes the total Ohio school district tax liability, the SD 101 concentrates on the remittance of withheld school district income taxes, showcasing another layer of tax responsibility for Ohio employers.

The IRS form 940, used for the Federal Unemployment Tax Act (FUTA) tax reporting, parallels the Ohio IT 3 form somewhat. The form 940 involves reporting on taxes paid into the federal unemployment tax system, reflecting an employer's annual financial obligations towards this scheme. This form, similar to the IT 3, demonstrates the importance of employer contributions to federal and state tax and employment programs, ensuring that unemployment insurance systems are adequately funded.

Another IRS form, W-3, the Transmittal of Wage and Tax Statements, is closely related to the Ohio IT 3 form. The W-3 is utilized to submit all W-2 forms for a business to the Social Security Administration. The purpose aligns with that of the IT 3 in aggregating and transmitting employee wage and tax information, although the W-3 serves as a federal conduit, further emphasizing the synergy between state and federal tax reporting practices.

The Employer's Annual Federal Tax Return (form 944) is designed for smaller employers to report their employees' withheld federal income tax and the employer's portion of Social Security and Medicare taxes. Although aimed at a narrower audience, the parallels with the Ohio IT 3 form's goals of tax reporting and compliance remain evident, underscoring the broader framework of employer reporting obligations across various tax domains.

Lastly, the Ohio IT 1040 form, which is the Individual Income Tax Return form for Ohio residents, indirectly correlates with the information contained within the Ohio IT 3 form. While the IT 3 deals with the collection and reporting of employment taxes at the employer level, the IT 1040 form represents the culmination of an individual's state tax reporting process. Together, they encapsulate the cycle of tax documentation from earnings reporting to personal tax submission in the state of Ohio.

When preparing the Ohio IT 3 form for submission, it's important to understand and follow specific guidelines to ensure the process is completed accurately and efficiently. Here's a list of dos and don'ts to help you navigate the process:

Following these guidelines will help in preparing and submitting the Ohio IT 3 form correctly, thus fulfilling your obligations under Ohio law.

Understanding the Ohio IT 3 Transmittal of W-2 and 1099-R Statements is key to ensuring compliance with the state's requirements for reporting employee and retiree income. However, several misconceptions can lead to errors in the filing process. Let's clarify four common misunderstandings:

Understanding these key aspects of the Ohio IT 3 form can significantly streamline the filing process and ensure compliance with state taxation requirements. By avoiding these common misconceptions, employers can fulfill their reporting obligations accurately and timely.

Filing the Ohio IT 3 form correctly and on time is pivotal for employers to ensure compliance with state tax obligations. Here are eight key takeaways about how to handle this important document:

Understanding these key aspects of the Ohio IT 3 form can significantly streamline the process of filing wage and tax statements, ensuring compliance with Ohio state tax laws and regulations. It's a clear signal from the Ohio Department of Taxation that modernization through electronic filing is not only preferred but, in many cases, required. Employers should adapt to this approach, leveraging the benefits of efficiency, accuracy, and security that electronic filing provides.

Warren Juvenile Court - Mandatory for the form to be typewritten or filled in ink and requires detailed information about the child or children involved.

Ohio Historical Society - It embodies the state's respect for its history and its commitment to future generations, ensuring that valuable records are preserved in the public interest.