Blank Ohio It 4708 Template

Blank Ohio It 4708 Template

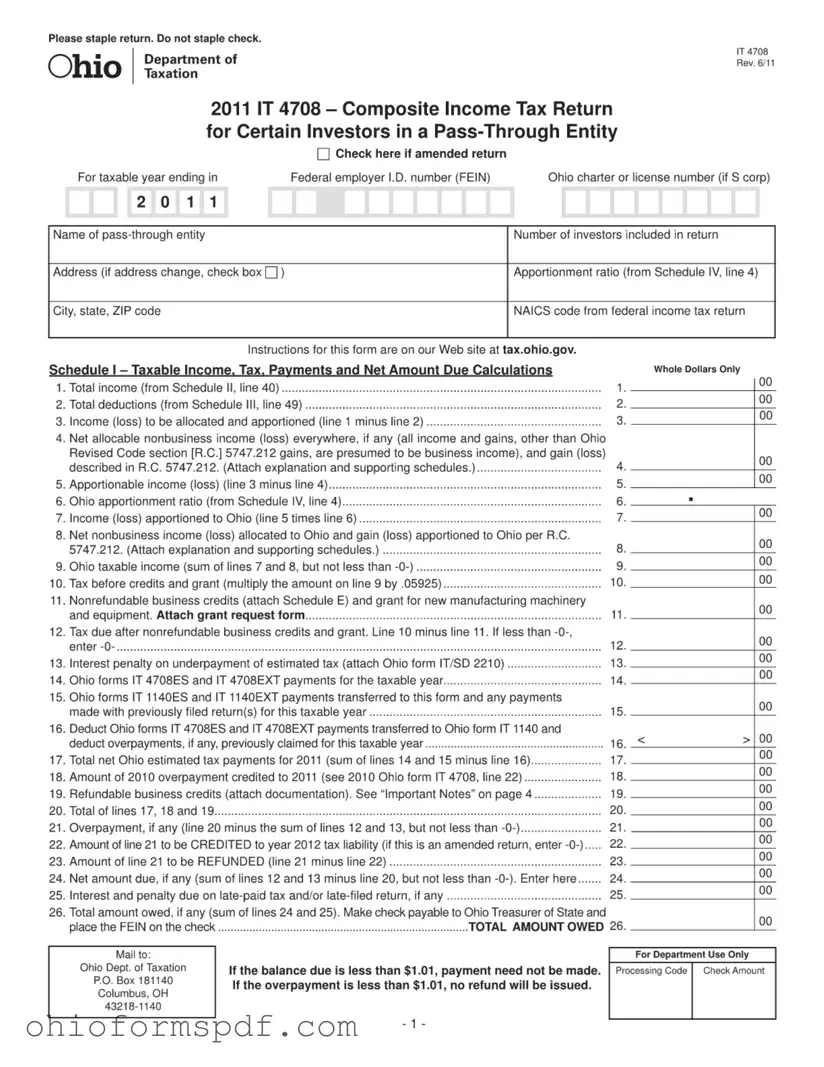

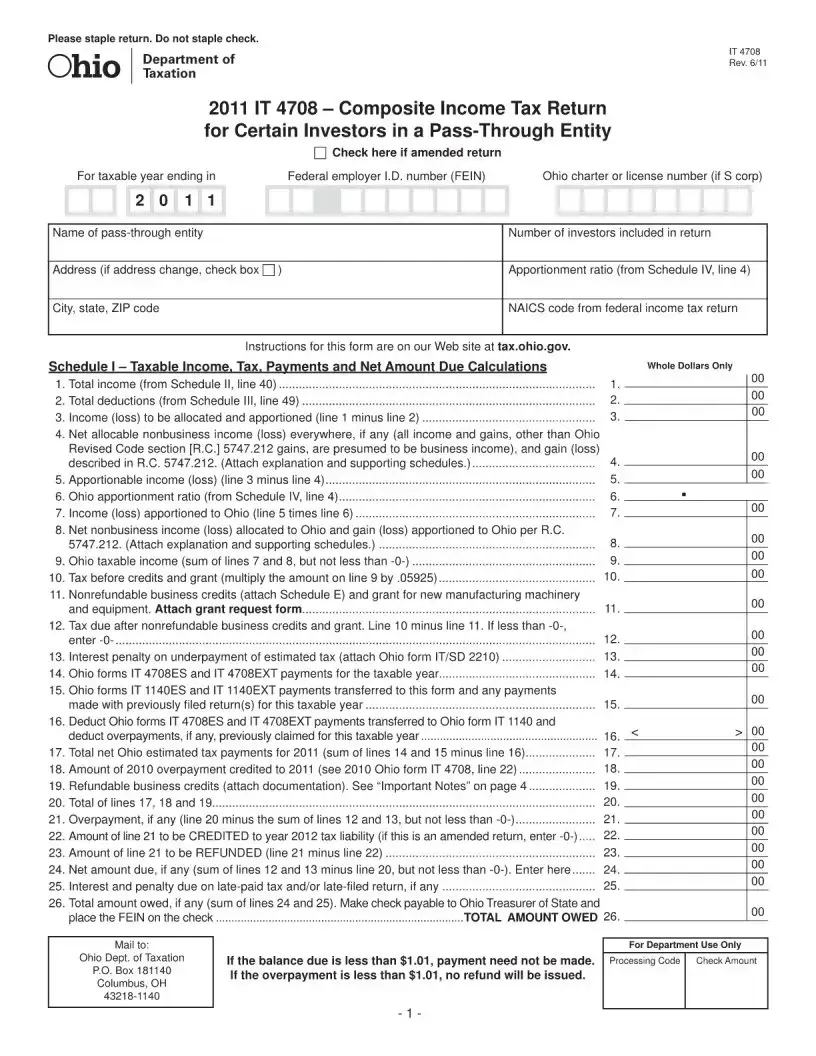

In the state of Ohio, one key document that stands out for its role in tax filings for certain entities is the Ohio IT 4708 form. Designed with the specific purpose of addressing the composite income tax obligations of pass-through entities (PTEs) such as partnerships, S corporations, and limited liability companies (LLCs) that opt to file on behalf of their investors or members, this form encapsulates various aspects of tax computation and reporting that are crucial for ensuring compliance with state tax laws. Key features of the form include the provision for the entity to report and pay composite income tax due on behalf of qualifying investors, details on income apportionment, and calculations for both resident and nonresident investors. Notably, by utilizing the IT 4708 form, entities can streamline the tax filing process, potentially simplifying the compliance landscape for investors who otherwise would have to file individual state income tax returns. This mechanism not only aids in the efficient administration of tax but also underscores Ohio’s approach to managing tax obligations in a way that balances the needs of the state with the operational realities of modern business structures.

| Fact Name | Description |

|---|---|

| Purpose | The Ohio IT 4708 form is used for reporting income or losses by pass-through entities, such as partnerships and S corporations, that have investors in Ohio. |

| Governing Law | This form is governed under the laws of the State of Ohio, specifically under the Ohio Revised Code that deals with taxation of pass-through entity income. |

| Filing Requirement | Pass-through entities with Ohio investors are required to file Form IT 4708 to report the entity's income, deductions, and credits to the State of Ohio. |

| Due Date | The form is typically due on the 15th day of the fourth month following the end of the entity's taxable year. For most entities operating on a calendar year, this would be April 15th. |

| Penalties | Entities that fail to file on time, incorrectly report income, or underpay taxes may be subject to penalties and interest as determined by the Ohio Department of Taxation. |

Filling out the Ohio IT 4708 form is an essential task for many, ensuring correct financial processes are followed. This form might seem daunting at first, but breaking it down into steps makes the process more manageable. For those unfamiliar, the Ohio IT 4708 form is pivotal in reporting certain types of income. To complete it accurately, one needs to follow a structured approach. Here’s a step-by-step guide to help navigate through the form, smoothing the path towards achieving compliance with Ohio's financial regulations.

After completing these steps, it’s a waiting game. The submission of the Ohio IT 4708 form is a significant step in maintaining financial responsibility. Once submitted, ensure to keep a copy of the form and any supporting documents for your records. Staying organized and retaining these documents help in tracking financial standings and are crucial for reference in case of queries or audits in the future.

What is the Ohio IT 4708 form?

The Ohio IT 4708 form is a tax document specifically designed for pass-through entities, such as partnerships or S corporations, that have investors or owners needing to report their share of the income or losses from Ohio sources. It enables the entity to file a composite return on behalf of certain investors or owners who are non-residents of Ohio.

Who needs to file the Ohio IT 4708 form?

Any pass-through entity that has income from Ohio sources and has one or more investors or owners who are non-residents of Ohio must file the IT 4708 form. This requirement holds unless all non-resident owners have signed an agreement to file their own individual Ohio tax returns.

What information is required on the IT 4708 form?

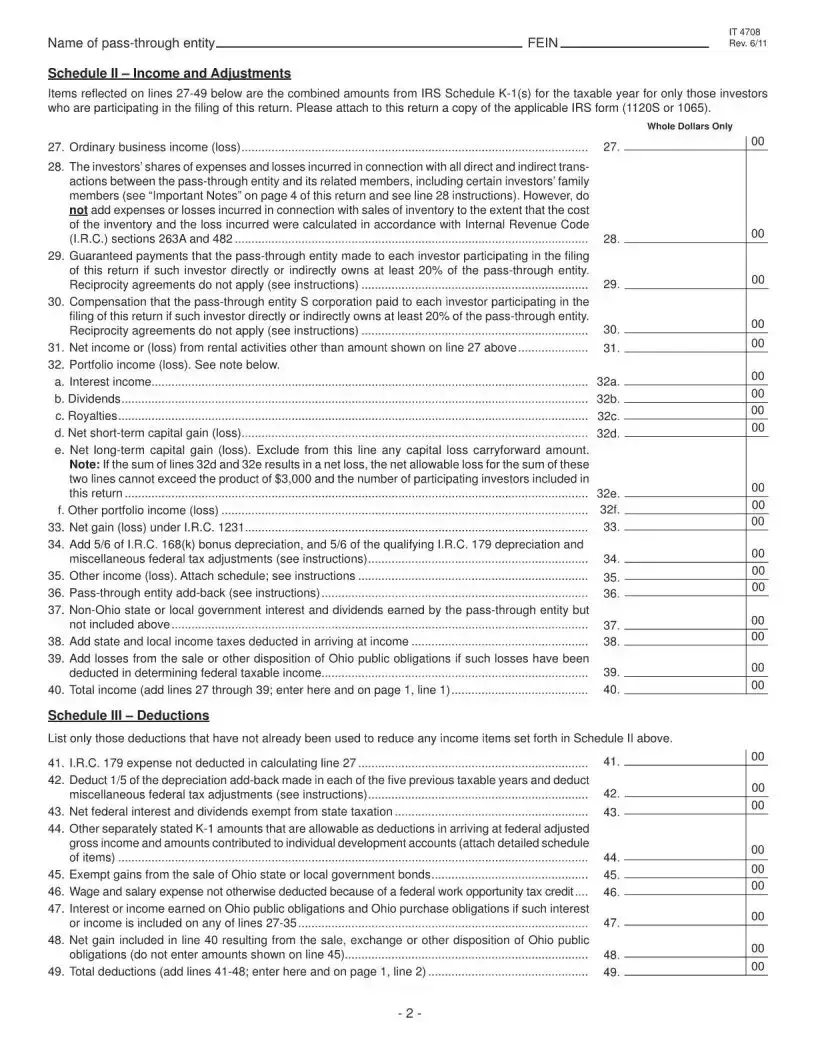

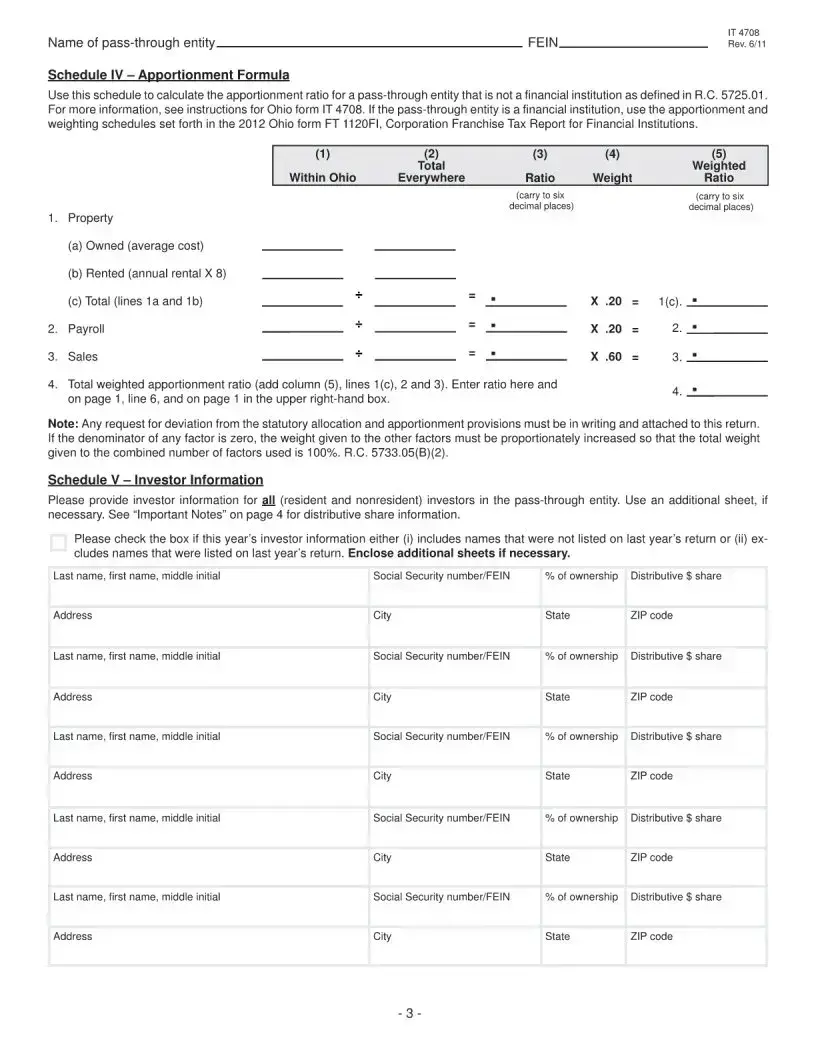

The form requires detailed information about the pass-through entity's income from Ohio sources, distributions to each non-resident owner, and the total tax due. It also requires the identification of each participating non-resident owner, including their name, Social Security Number (or Federal Identification Number), and the share of income or loss attributed to them.

When is the IT 4708 form due?

The IT 4708 is due on the 15th day of the fourth month following the end of the taxable year for the pass-through entity. For most entities operating on a calendar year, this means the deadline is April 15th of the following year.

How is the tax calculated on the IT 4708 form?

Tax is calculated based on the total adjusted income of the pass-through entity from Ohio sources allocated to all participating non-resident owners at the applicable individual or corporate tax rate, depending on the nature of the income. Specific credits, deductions, and payment of estimated taxes can also impact the final tax due.

What if some non-resident owners file their own Ohio tax returns?

If some non-resident owners choose to file their own Ohio tax returns, the pass-through entity should not include their share of the income or taxes due for those individuals on the IT 4708 form. These owners must provide a written consent, using Form IT 4708UP, indicating their agreement to file their own return and their understanding that they are separately responsible for their Ohio tax obligations.

Are there penalties for late filing or payment?

Yes, Ohio may impose penalties for both late filing of the IT 4708 form and late payment of any taxes due. These penalties are calculated as a percentage of the unpaid tax and increase the longer the delay. Additionally, interest may accrite on any unpaid tax from the due date until the tax is fully paid.

Can the IT 4708 form be filed electronically?

Yes, Ohio supports electronic filing for the IT 4708 form, offering a more convenient and faster processing option than paper filing. Electronic filing can also help reduce errors, ensuring a smoother handling of your tax obligations.

When completing the Ohio IT 4708 form, people often encounter a few common stumbling blocks. This form, essential for reporting certain types of income, requires careful attention to detail. Understanding where others have faltered can guide you to a smoother filing process. Below are eight common mistakes made:

Not checking the correct tax year box at the top of the form. It may seem basic, but ensuring the correct tax year is indicated is a fundamental step that is frequently overlooked.

Entering incorrect information for the entity. Whether it's a miswritten EIN (Employer Identification Number) or the wrong entity name, such mistakes can lead to processing delays or even misfiled returns.

Skipping the apportionment questions. These are crucial for determining how income is divided and taxed among various states.

Miscalculating the income or loss. This often happens due to overlooking certain deductions or not properly applying tax codes. Getting these numbers right is essential for an accurate return.

Forgetting to sign and date the return. This might seem surprising, but many returns are submitted without the necessary signatures, leading to automatic rejections.

Omitting required attachments. Attachments may include schedules detailing income or documents verifying credits. Failure to include these can halt the processing of your return.

Not using the correct version of the form. Tax codes and forms can change from year to year. Using an outdated form can cause significant issues.

Incorrect payment information. This includes both overpayments and underpayments and can result from calculation errors or misunderstanding of tax obligations.

Avoiding these common mistakes requires a careful and methodical approach to filling out the Ohio IT 4708 form. Always double-check your information, confirm that you're using the most current form version, and ensure you've understood the instructions provided. When in doubt, consulting with a professional can provide clarification and peace of mind.

When dealing with the Ohio IT 4708 form, which is essentially focused on taxes for pass-through entities that have to report their income at the entity level, several other documents often come into play. These documents ensure that the information provided is accurate, complete, and in compliance with Ohio's tax regulations. They might be used for various purposes such as substantiating claims, providing detailed financial information, or even for personal identification. Below is a list of some commonly used forms and documents with the Ohio IT 4708 form, along with brief descriptions of each.

Understanding and gathering these documents can significantly streamline the tax filing process for pass-through entities and their members. It's important to keep detailed records and prepare all necessary forms accurately to ensure compliance with both state and federal tax codes. Individuals and entities are encouraged to seek professional advice or assistance if they are unsure about any requirements or need help with their tax preparation.

The Ohio IT 4708 form is closely related to the IRS Form 1065, which is the U.S. Return of Partnership Income. Both forms are used to report the income, gains, losses, deductions, and credits of a business entity. While the Ohio IT 4708 is specific to reporting the adjustments required for pass-through entities' composite income tax in Ohio, the IRS Form 1065 serves a similar purpose at the federal level for partnerships, detailing how the profits and losses are divided among partners.

Another similar document is the IRS Schedule K-1 (Form 1065), which complements the IRS Form 1065. The Schedule K-1 is used to report each partner's share of the partnership's earnings, losses, deductions, and credits. Like the Ohio IT 4708, which deals with income allocation for tax purposes, Schedule K-1 ensures that the partnership's income is reported correctly on each partner's individual tax return, reflecting state-level adjustments in the case of Ohio IT 4708.

The Ohio IT 1140 form, Partnership and S Corporation Withholding Tax Return, shares similarities with the Ohio IT 4708 as both are concerned with pass-through entities in Ohio. While the IT 4708 is specifically for composite return purposes, detailing adjustments to income for nonresident individuals, the IT 1140 form addresses withholding tax obligations for partnerships and S corporations, showcasing different aspects of tax responsibilities for these entities within Ohio.

Form 1041, U.S. Income Tax Return for Estates and Trusts, also bears resemblance to the Ohio IT 4708 form in its function of reporting income for a specific type of entity. Although Form 1041 addresses estates and trusts at the federal level, and the Ohio IT 4708 focuses on pass-through entities' income at the state level, both serve to detail how income is distributed or retained within the entity, affecting how taxes are computed and filed.

The California Form 565, Partnership Return of Income, is akin to the Ohio IT 4708 in serving a similar function for partnerships in the state of California. Just as the Ohio IT 4708 addresses Ohio state tax implications for pass-through entities, California Form 565 deals with reporting income, deductions, and credits for partnerships operating within California, emphasizing the state-specific approach to tax reporting for entities.

Another document closely related to the Ohio IT 4708 is the New York IT-204-CP, Partnership, and New York S Corporation Franchise Tax Return for Composite Filers. This form is used by partnerships and S corporations in New York for composite filing, much like the Ohio IT 4708 allows composite filing for similar entities in Ohio. Both forms accommodate a joint filing approach for nonresident members to simplify state income tax compliance.

Finally, the IRS Form 1120S, U.S. Income Tax Return for an S Corporation, shares a purpose with the Ohio IT 4708 in that it is designed for reporting income, losses, and dividends of S corporations. Although Form 1120S is a federal form and the Ohio IT 4708 is state-specific, they each cater to pass-through entities, ensuring that income is accurately reported for tax calculation purposes, with the primary difference being the level of government to which they are submitted.

Filling out the Ohio IT 4708 form, also known as the "Pass-Through Entity and Trust Withholding Tax Return," is a necessary step for certain entities operating within Ohio. Like any tax form, it requires careful attention to detail and an understanding of the applicable regulations. To navigate this process smoothly, here are ten critical dos and don'ts:

By following these tips, entities can more confidently navigate the process of completing the Ohio IT 4708 form, ensuring compliance with state tax obligations in an efficient and accurate manner.

When it comes to tax documentation and compliance, clarity is key. The Ohio IT 4708 form, specifically designed for pass-through entities to report and pay their composite income tax, is no exception. However, there are several misconceptions that often lead to confusion among taxpayers. Let's clarify some of the common misunderstandings surrounding this form.

Understanding these misconceptions about the Ohio IT 4708 form can greatly improve tax compliance and efficiency for pass-through entities and their investors. Accurate knowledge ensures that entities can plan appropriately and avoid pitfalls associated with incorrect filings or misunderstood obligations.

In Ohio, the IT 4708 form serves as an essential document for pass-through entities, such as partnerships and S corporations, to report and pay the state's composite income tax on behalf of their investors. When preparing and submitting this form, there are several crucial considerations to keep in mind to ensure compliance with state tax regulations:

By keeping these key points in mind, pass-through entities can navigate the process of completing and submitting the Ohio IT 4708 form more effectively, ensuring they meet their tax obligations while minimizing burdens on their investors.

Jfs Forms - Equipped with a straightforward authorization section, the form simplifies legal compliance for information release, ensuring a seamless verification process.

Ohio Bwc Permanent Total Disability - For the form to be processed, the signed and dated copy must be correctly submitted to the appropriate office.