Blank Ohio It 942 Template

Blank Ohio It 942 Template

Understanding the intricacies of Ohio's tax filing and withholding processes is essential for employers and employees alike. The Ohio IT-942 form, serving as a crucial component of these procedures, facilitates the quarterly reconciliation of withheld state income tax, ensuring accuracy and compliance with state tax laws. This comprehensive document caters to various facets of withholding account maintenance, beginning with a detailed exploration of field descriptions and followed by in-depth instructions designed to guide users through each step of the process with clarity. It covers a wide range of operations from adding or deleting accounts, navigating through the Ohio IT-501 wizard, to conducting monthly and quarterly information reviews, including an overview of balance due procedures. Moreover, it extends into the realms of school district-related financial transactions, emphasizing the necessity of updating district information and associating withholding account numbers with specific companies or Federal Employer Identification Numbers (FEIN). Essential for accurate tax reporting and payments, the guide also delves into mechanisms for making different types of payments, including billing notice and assessment payments. By adhering to the guidelines outlined in the Ohio IT-942 form and its accompanying sections, entities can ensure compliance, streamline tax reporting efforts, and maintain accurate records of withholding tax obligations.

Table of Contents

WITHHOLDING ACCOUNT MAINTENANCE |

.......................3 |

Field Descriptions |

3 |

Instructions |

4 |

ADDING AN ACCOUNT |

5 |

Rules for Adding Accounts |

5 |

Instructions |

.............. 5 |

DELETE AN ACCOUNT |

8 |

OHIO IT ‐ 501 WIZARD |

10 |

IT ‐ 501 |

11 |

Field Descriptions |

12 |

Instructions |

12 |

IT ‐ 501 REVIEW FILING INFORAMTION PAGE |

13 |

Field Descriptions |

13 |

Instructions |

14 |

OHIO |

15 |

Field Descriptions |

15 |

Instructions |

16 |

IT – 941 MONTHLY INFORMATION |

17 |

Field Descriptions |

18 |

Instructions |

18 |

IT – 941 BALANCE DUE |

... 19 |

Field Descriptions |

... 19 |

Instructions |

20 |

IT – 941 REVIEW |

21 |

Field Descriptions |

22 |

Instructions |

23 |

OHIO IT‐942 WIZARD |

24 |

Field Descriptions |

24 |

Instructions |

25 |

IT‐942 QUARTERLY INFORMATION |

26 |

Field Descriptions |

27 |

Instructions |

27 |

IT‐942 BALANCE DUE |

28 |

Field Descriptions |

28 |

Instructions |

29 |

IT‐942 REVIEW |

30 |

Field Descriptions |

31 |

Instructions |

31 |

IT‐942 4TH QUARTERLY/ANNUAL RECONCILIATION |

33 |

Field Descriptions |

33 |

Instructions |

34 |

User Guide |

Withholding |

6/20/2007 |

IT‐942 4TH QUARTER INFORMATION |

35 |

|

Field Descriptions |

...................... 36 |

|

Instructions |

...................... 36 |

|

IT‐942 4TH QUARTER BALANCE DUE |

...................... 37 |

|

Field Descriptions |

...................... 37 |

|

Instructions |

...................... 38 |

|

IT‐942 4TH QUARTER REVIEW |

...................... 40 |

|

Field Descriptions |

...................... 41 |

|

Instructions |

............ 42 |

|

OHIO SD‐101 WIZARD |

..................... 44 |

|

Field Descriptions |

...................... 44 |

|

Instructions |

...................... 45 |

|

SD‐101 WITHHOLDING INFORMATION |

...................... 46 |

|

Field Descriptions |

...................... 47 |

|

Instructions |

...................... 48 |

|

SD‐101 REVIEW |

...................... 49 |

|

Field Descriptions |

...................... 50 |

|

Instructions |

...................... 51 |

|

ADDING/REMOVING SCHOOL DISTRICTS |

..................... 52 |

|

Field Descriptions |

...................... 52 |

|

Instructions |

............ 53 |

|

OHIO SD‐141 WIZARD |

..................... 56 |

|

Field Descriptions |

...................... 56 |

|

Instructions |

...................... 57 |

|

SD‐141 WITHHOLDING INFORMATION |

...................... 59 |

|

Field Descriptions |

...................... 60 |

|

Instructions |

...................... 61 |

|

SD‐141 REVIEW |

...................... 63 |

|

Field Descriptions |

...................... 64 |

|

Instructions |

...................... 66 |

|

MAKING PAYMENTS |

..................... 67 |

|

BILLING NOTICE PAYMENT |

...................... 67 |

|

Field Descriptions |

...................... 67 |

|

Instructions |

68 |

|

ASSESSMENT PAYMENT |

69 |

|

Field Descriptions |

69 |

|

Instructions |

70 |

|

PAYMENT ONLY |

71 |

|

Field Descriptions |

71 |

|

Instructions |

72 |

|

Table of Contents |

Page 2 |

User Guide |

Withholding |

6/20/2007 |

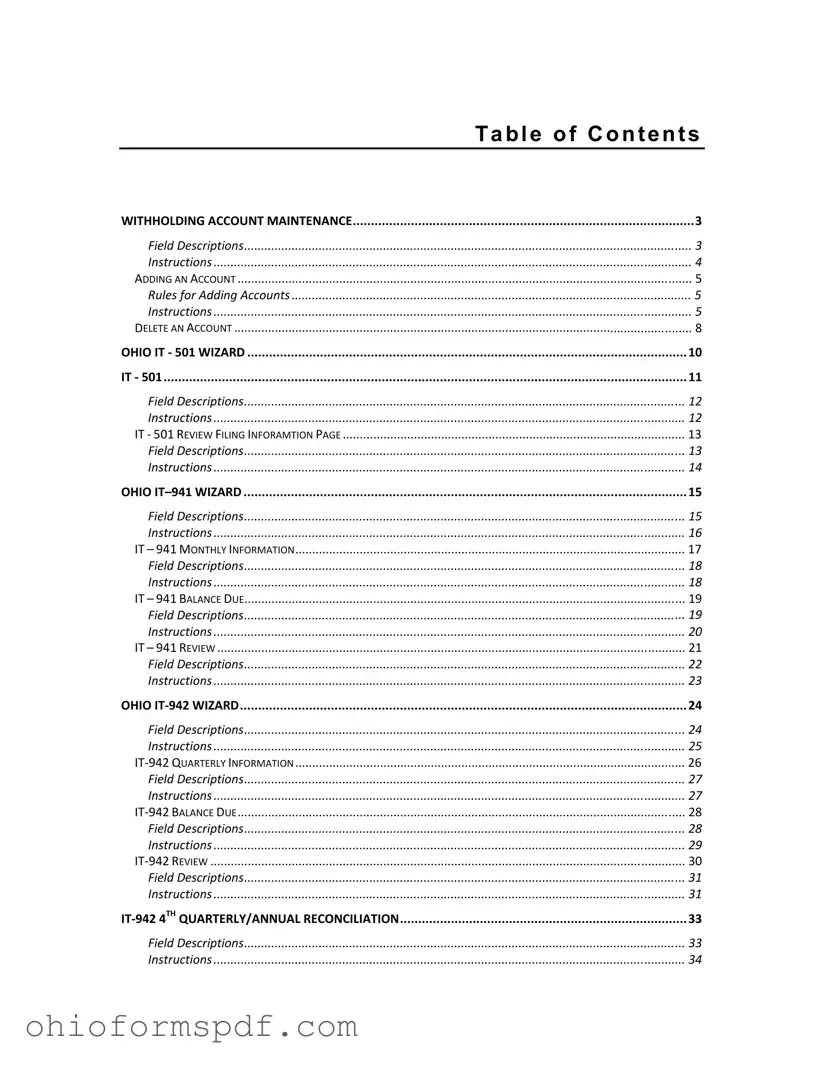

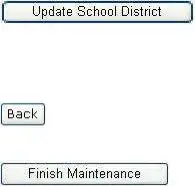

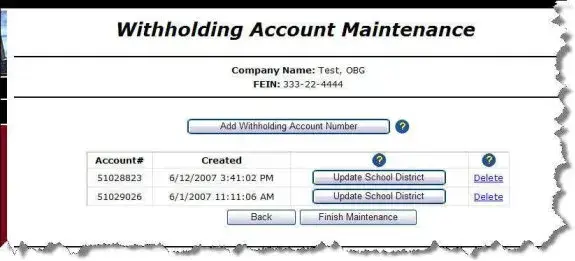

Withholding Account Maintenance

Use the Withholding Account Maintenance page to:

•Review existing withholding account information

•Associate a withholding account number to a specific Company/FEIN

•Update School District information

Field Descriptions

Field Name |

Description |

|

|

Company Name |

The name of the company. |

|

|

FEIN |

Federal Employer Identification |

|

Number associated with the |

|

company name. |

|

|

|

Opens the Withholding Account Set |

|

Up Wizard. |

|

|

Account # |

A list of account numbers |

|

currently associated with the |

|

|

Withholding Account Maintenance |

Page 3 |

User GuideWithholding6/20/2007

|

Field Name |

Description |

|

|

|

|

|

Company Name. |

|

|

|

|

Created |

The date on which the account |

|

|

number was created. |

|

|

|

|

|

Opens the Update School District |

|

|

page. |

|

|

|

|

Delete |

When selected, this link removes |

|

|

the account number from the |

|

|

Company profile. |

|

|

|

|

|

Returns to the Ohio Withholding |

|

|

Progress Page without updating any |

|

|

information. |

|

|

|

|

|

Saves the information on the page |

|

|

and returns to the Ohio |

|

|

Withholding Progress Page. |

|

|

|

Instructions |

|

|

•

•

•

Select  to display the Withholding Account

to display the Withholding Account

Select  to display the Update School Districts page (see page 52 for instructions).

to display the Update School Districts page (see page 52 for instructions).

Select the Delete link to remove an account from the list. The system displays the Confirm Delete Account page.

•When you are finished making changes to your company profile click  . The system saves the information and returns to the Ohio Withholding Progress Page.

. The system saves the information and returns to the Ohio Withholding Progress Page.

Withholding Account Maintenance |

Page 4 |

User Guide |

Withholding |

6/20/2007 |

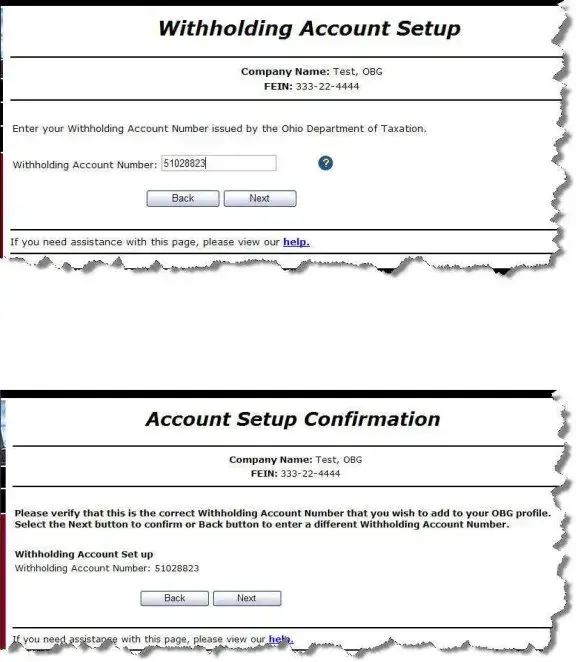

Adding an Account

Use the Withholding Account

Rules for Adding Accounts

•

•

Every account must be at least 8 characters in length.

Every Company/FEIN must have at least one account associated with it to file withholding reports.

Instructions

•Select “Maintain Withholding Account Number” from the drop down list

on the Ohio Withholding Progress Page and click  . The system displays the Withholding Account Maintenance page.

. The system displays the Withholding Account Maintenance page.

•Click  . The system displays the Withholding Account Setup page.

. The system displays the Withholding Account Setup page.

Withholding Account Maintenance |

Page 5 |

User Guide |

Withholding |

6/20/2007 |

•

•

•

Enter the Withholding Account Number you want to add.

Click  . The system asks you to verify that you want to add this account number to your profile.

. The system asks you to verify that you want to add this account number to your profile.

Click  to verify that you want to add this account number to your profile. The system returns to the Withholding Account Maintenance page and displays the added account number in your list of profile accounts.

to verify that you want to add this account number to your profile. The system returns to the Withholding Account Maintenance page and displays the added account number in your list of profile accounts.

Withholding Account Maintenance |

Page 6 |

User Guide |

Withholding |

6/20/2007 |

•

•

Verify that the account number displayed on the page is the account number you want to add to the Company Name/ FEIN shown at the top of the page.

Click  to return to the Ohio Withholding Progress Page.

to return to the Ohio Withholding Progress Page.

Withholding Account Maintenance |

Page 7 |

User Guide |

Withholding |

6/20/2007 |

Delete an Account

You may remove a withholding account from your Company profile using the Withholding Account Maintenance page. Removing the account from your profile does not delete the account completely, it only removes it from your filings with the OBG. You may only delete/cancel an account permanently during the final withholding filing process.

•Click the Delete link on the Withholding Account Maintenance page. The system displays the Confirm Delete Account page.

•Verify that the information displayed on the Confirm Delete Account page is correct.

Withholding Account Maintenance |

Page 8 |

User Guide |

Withholding |

6/20/2007 |

Action |

Result |

|

|

|

The system removes the account from the Withholding |

|

Account Maintenance page. |

|

The system does not remove the account and returns |

|

to the Withholding Account Maintenance page. |

|

|

Withholding Account Maintenance |

Page 9 |

User Guide |

Withholding |

6/20/2007 |

Ohio IT - 501 Wizard

The OBG system uses a “Wizard” process to make the IT - 501 form eaier to complete. This Wizrd steps you through the process of answering a few simple questions and filling in the blanks provided. The Wizard follows the following process:

Ohio IT - 501 Wizard |

Page 10 |

| Fact | Description |

|---|---|

| Purpose of Form | The Ohio IT-942 form is used for quarterly reconciliation of withholding taxes. |

| User Guide Publication Date | The user guide for Withholding Account Maintenance, which includes the IT-942 form, was published on 6/20/2007. |

| Withholding Account Maintenance | Allows users to review existing withholding account information, associate a withholding number to a company, and update school district information. |

| Adding an Account | To add an account, a withholding account number must be issued by the Ohio Department of Taxation (ODT) and associated with a specific Company Name/FEIN. |

| Rule for Accounts | Each account must be at least 8 characters in length, and every Company/FEIN must have at least one account for filing withholding reports. |

| Governing Law | The Ohio IT-942 form and related withholding processes are governed by Ohio state tax laws. |

| Form Sections | The IT-942 form includes sections for quarterly information, balance due, and review, culminating with a 4th quarter/annual reconciliation. |

Filling out the Ohio IT-942 form is an important step for businesses at the end of the year or quarter. This form is used for reconciling withholding tax amounts. Correctly completing and submitting this form ensures that businesses are compliant with Ohio tax laws and regulations. Here are the steps to fill out the form accurately:

Once you have filled out the form completely and reviewed all the information for accuracy, submit it according to the instructions provided by the Ohio Department of Taxation. Timely and correct submission of the IT-942 helps maintain your company's good standing and compliance with state tax obligations.

What is the Ohio IT 942 form?

The Ohio IT 942 form is a quarterly withholding reconciliation form used by businesses to reconcile the amount of Ohio state income tax withheld from employees' wages throughout the quarter with the total tax reported and paid to the Ohio Department of Taxation.

Who needs to file the Ohio IT 942 form?

Any business that withholds Ohio state income tax from employees' wages must file the Ohio IT 942 form on a quarterly basis to reconcile their withholdings.

When is the Ohio IT 942 form due?

This form is due on the last day of the month following the end of each quarter. For example, for the first quarter (January - March), the form is due by April 30th.

How do I add an account in the Ohio withholding account maintenance section?

To add an account, select "Maintain Withholding Account Number" from the drop-down list on the Ohio Withholding Progress Page and then click. Follow the instructions provided on the Withholding Account Setup page that appears.

Can I delete an account in the Ohio withholding account maintenance section?

Yes, you can delete an account by selecting the Delete link next to the account number you wish to remove. After clicking, you will be prompted to confirm the deletion.

What information is required to fill out the Ohio IT 942 form?

You'll need your company name, the Federal Employer Identification Number (FEIN), and detailed quarterly withholding tax information, including the total amount of tax withheld from employees' wages and any adjustments to be made.

Is there a penalty for filing the Ohio IT 942 form late?

Yes, late filings may result in penalties and interest charges. The specific amounts will depend on how late the form is filed and the amount of tax that was due.

How can I obtain a withholding account number if I'm new to filing in Ohio?

Contact the Ohio Department of Taxation (ODT) to obtain a new withholding account number. Only the ODT can issue these numbers to businesses.

Can I file the Ohio IT 942 form electronically?

Yes, electronic filing is available and encouraged for faster processing and convenience. Check the Ohio Department of Taxation's website for electronic filing options.

What should I do if I made a mistake on a previously filed Ohio IT 942 form?

If you discover an error on a previously filed IT 942 form, you should file an amended return as soon as possible. Detailed instructions on how to file an amended return are available from the Ohio Department of Taxation.

When filling out the Ohio IT-942 form, people often make mistakes due to overlooking details or misunderstanding the form's requirements. Here are nine common errors:

Making these mistakes can have a range of consequences, from minor administrative hassles to significant legal and financial penalties. It is crucial to approach the task of filling out the Ohio IT-942 form with care and attention to detail.

When dealing with Ohio's payroll and withholding tax requirements, businesses often need to complete and file several forms in addition to the Ohio IT-942 form. Such documents are key to maintaining compliance with the state's tax laws. Understanding each document's purpose is crucial for timely and accurate tax filing.

These documents together form a comprehensive framework for managing and reporting payroll taxes in Ohio. Proper understanding and utilization of each form not only facilitate compliance with tax regulations but also streamline the tax reporting process for employers. Keeping abreast of filing deadlines and requirements for each form can significantly ease the administrative burden of payroll tax management.

The Ohio IT-941 form, pertaining to monthly withholding information, shares similarities with the Ohio IT-942 form. Both serve as crucial elements in the process of reporting and remitting withheld taxes. The IT-941 form operates on a monthly basis, emphasizing periodic reporting, whereas the IT-942 is utilized for quarterly declarations. The common ground between these forms lies in their focus on ensuring accurate tax withholdings are reported and paid by employers, albeit on different schedules.

Similar to the Ohio IT-942 form, the Ohio SD-101 serves a specific purpose in withholding tax documentation, targeting school district withholding details. This form is specially designed for reporting taxes withheld on behalf of employees to local school districts. The simultaneous requirement for precision in recording withholdings connects the SD-101 closely with the IT-942, as both demand detailed financial information to comply with state and local tax regulations.

The process outlined in the Adding/Removing School Districts section is notably akin to the method described in the Ohio IT-942 for managing withholding account specifics. These segments guide users through adjustments in account details, be it for a school district or a general tax withholding purpose. Here, the essence lies in administrating tax-related data to maintain up-to-date records for compliance and accurate filing, showcasing the administrative parallels between managing school district information and quarterly tax withholdings.

The Ohio SD-141, like the IT-942, plays an integral role in facilitating tax administrative tasks. The SD-141 form is used for annual reconciliation of school district taxes withheld, analogous to the IT-942's function for quarterly tax reconciliation. Both documents necessitate a year-end or period-end review of tax amounts withheld versus amounts due, ensuring entities have appropriately met their taxation obligations.

The IT-942 4th Quarterly/Annual Reconciliation process bears resemblance to procedures found in other tax reconciliation practices, such as those for federal Form W-2 and W-3 reporting. This comparison arises from the need to reconcile and report the total amount of taxes withheld from employees with amounts actually remitted to the tax authority, serving as a check to ensure that withholdings are accurately reported and submitted for both state and federal taxes.

The Withholding Account Maintenance section in the IT-942 documentation resembles features found in general payroll software platforms. These systems offer functionalities for adding, updating, and deleting account information, mirroring the manual process detailed in the IT-942 guide. The core objective is managing business and employee information effectively to comply with tax withholding requirements, whether through automated software or manual entry.

The Billing Notice Payment instructions within the IT-942 documentation share similarities with procedures for managing notices and penalties in tax software or compliance systems. Such sections provide guidance on responding to specific tax notices, including payments for underreported taxes or penalties, drawing parallels in the handling of tax compliance issues across different platforms and forms.

Making Payments, as outlined in relation to the IT-942 form, is a fundamental task that aligns closely with functionalities seen in online tax payment systems used by federal and state tax authorities. The focus is on ensuring timely and accurate tax payments, a commonality shared across many tax-related documents and systems. This involves confirming the correct amounts are paid to the appropriate tax entity to avoid underpayment penalties.

The Assessment Payment segment contains instructions which can be likened to similar procedures in handling audits, assessments, or adjustments by tax authorities. Both in the context of the IT-942 form and broader tax practices, responding to assessments involves reviewing the tax authority's findings and remitting any additional amounts owed, ensuring tax compliance is maintained.

Finally, the concept of Payment Only submissions, as noted in the IT-942 documentation, is commonly encountered in direct tax payment arrangements across various tax forms and systems. This approach allows payers to make payments independent of regular filing schedules, commonly used for settling estimated taxes or addressing owed balances post-assessment, reflecting a flexible option for maintaining tax compliance.

When filling out the Ohio IT 942 form, there are several practices you should follow to ensure the process is smooth and error-free. Similarly, there are actions you should avoid to prevent common mistakes. Here is a concise guide to help you navigate the process efficiently.

5 Things You Should Do:

5 Things You Shouldn't Do:

By following these do's and don'ts, you can improve the accuracy of your Ohio IT 942 form submission and reduce the chances of encountering problems with your filing. Remember, the Ohio Department of Taxation's website is a valuable resource for additional guidance and support as you complete this process.

When it comes to understanding the Ohio IT-942 form, there are a few common misconceptions that can lead to confusion. Let's clear up some of these misunderstandings to make this process a bit easier.

By dispelling these myths, we hope to make the process of filing your Ohio IT-942 forms less intimidating. Whether you're a seasoned business owner or new to the responsibilities of tax filings, understanding the reality of these forms can help you manage your obligations more effectively.

Here are key takeaways for filling out and using the Ohio IT 942 form effectively:

Understanding these aspects of the Ohio IT 942 form ensures proper management of withholding accounts, contributing to a smoother tax filing process for businesses.

4 Points on License - Filing the BMV 2610 form is a proactive measure for eligible individuals in Ohio to enhance their security and protect against potential threats.

At What Age Do You Stop Paying Property Taxes in Ohio? - Clarifies legal obligations and processes for a minor’s name change, ensuring all actions are in the child's best interest.

How to Get Health Insurance License in Ohio - Applicants must designate an agent for service of process in each jurisdiction where they're applying, ensuring legal accountability.