Blank Ohio It Ar Template

Blank Ohio It Ar Template

In navigating the complexities of tax refunds within Ohio, residents are presented with the Ohio IT AR form, an essential document for individuals and school districts seeking refunds on their income taxes. This form, with its latest revision in September 2019, serves as a bridge for taxpayers who have already navigated the process of filing their Ohio income tax or school district income tax returns via forms Ohio IT 1040 or SD 100. Detailed in the form are sections requiring personal information, such as Social Security and contact numbers, alongside a comprehensive breakdown for calculating the refund requested. This calculation entails the inclusion of income tax withheld, estimated payments, any amounts previously settled with original or amended returns or an assessment, and refundable credits, leading to a conclusive refund amount prior to the calculation of any interest. Critically, the form mandates a declaration from the taxpayer, under penalty of perjury, affirming the accuracy and completeness of the application and accompanying documents, which are then directed to the Ohio Department of Taxation. Additionally, it reminds applicants of the mandatory disclosure of Social Security numbers, justified by federal and state legal provisions aimed at facilitating tax administration. The specificity and clarity provided in the Ohio IT AR form underscore its role as a crucial tool for taxpayers to assert their claims for refunds, guided by a structured format and clear instructions to ensure compliance and accuracy in submissions.

10211411

|

Tax Year |

|

IT AR |

|

|

|

|

|

Rev. 9/19 |

|

|

|

|

|

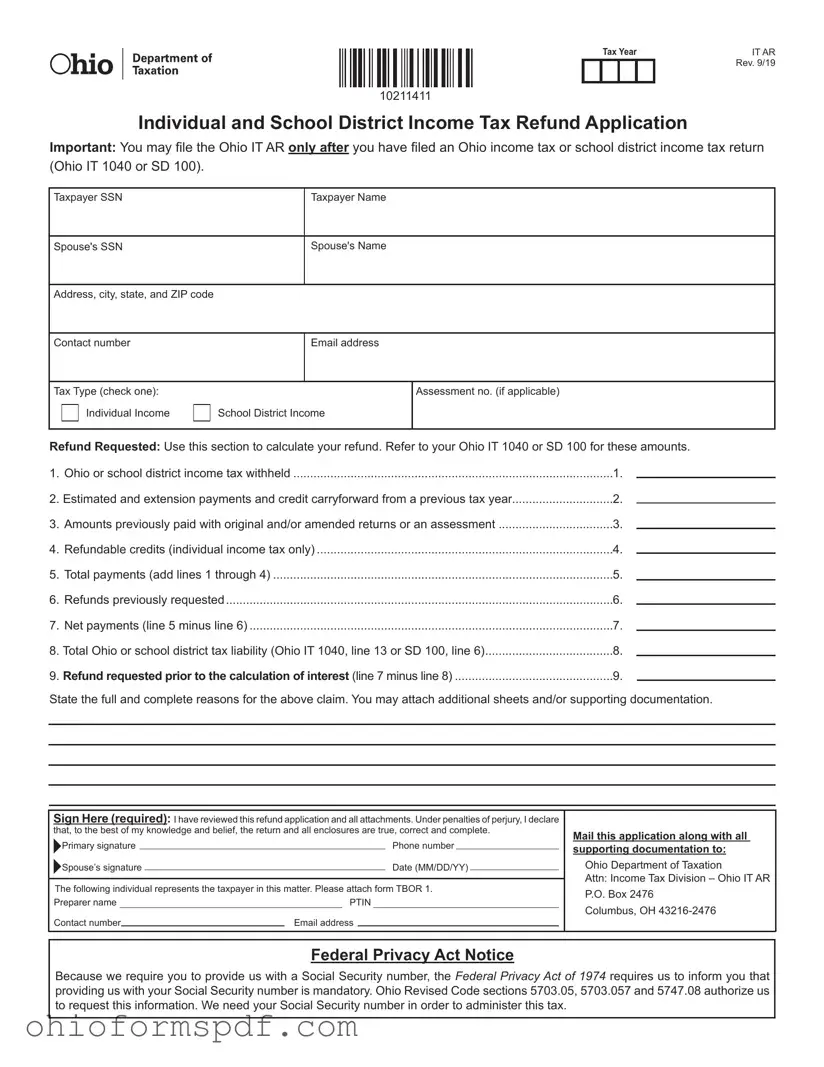

Individual and School District Income Tax Refund Application

Important: You may file the Ohio IT AR only after you have filed an Ohio income tax or school district income tax return (Ohio IT 1040 or SD 100).

Taxpayer SSN

Spouse's SSN

Taxpayer Name

Spouse's Name

Address, city, state, and ZIP code

Contact number

Email address

Tax Type (check one): Individual Income

School District Income

Assessment no. (if applicable)

Refund Requested: Use this section to calculate your refund. Refer to your Ohio IT 1040 or SD 100 for these amounts.

1. |

Ohio or school district income tax withheld |

1. |

2. |

Estimated and extension payments and credit carryforward from a previous tax year |

2. |

3. |

Amounts previously paid with original and/or amended returns or an assessment |

3. |

4. |

Refundable credits (individual income tax only) |

4. |

5. |

Total payments (add lines 1 through 4) |

5. |

6. |

Refunds previously requested |

6. |

7. |

Net payments (line 5 minus line 6) |

7. |

8. Total Ohio or school district tax liability (Ohio IT 1040, line 13 or SD 100, line 6) |

8. |

|

9. |

Refund requested prior to the calculation of interest (line 7 minus line 8) |

9. |

State the full and complete reasons for the above claim. You may attach additional sheets and/or supporting documentation.

|

Sign Here (required): I have reviewed this refund application and all attachments. Under penalties of perjury, I declare |

|

||||||||||||||

|

that, to the best of my knowledge and belief, the return and all enclosures are true, correct and complete. |

Mail this application along with all |

||||||||||||||

|

Primary signature |

|

|

|

|

|

|

|

Phone number |

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

supporting documentation to: |

||||

|

|

|

|

|

|

|

|

|

||||||||

|

Spouse’s signature |

|

|

|

|

|

|

Date (MM/DD/YY) |

|

|

Ohio Department of Taxation |

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Attn: Income Tax Division – Ohio IT AR |

|

The following individual represents the taxpayer in this matter. Please attach form TBOR 1. |

|||||||||||||||

|

P.O. Box 2476 |

|||||||||||||||

|

Preparer name |

|

|

|

PTIN |

|

|

|||||||||

|

|

|

Columbus, OH |

|||||||||||||

|

Contact number |

|

|

|

Email address |

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Federal Privacy Act Notice

Because we require you to provide us with a Social Security number, the Federal Privacy Act of 1974 requires us to inform you that providing us with your Social Security number is mandatory. Ohio Revised Code sections 5703.05, 5703.057 and 5747.08 authorize us to request this information. We need your Social Security number in order to administer this tax.

| Fact Name | Description |

|---|---|

| Form Designation | The correct designation for the form is Ohio IT AR, Rev. 9/19, which is used for Individual and School District Income Tax Refund Applications. |

| Filing Requirement | This form can be submitted only after the taxpayer has filed an Ohio income tax or school district income tax return, specifically Ohio IT 1040 or SD 100. |

| Refund Calculation Components | To calculate a refund, the form requires data on tax withheld, estimated payments, refundable credits for individual income tax, and previous payments or refunds requested. |

| Governing Laws | The Federal Privacy Act of 1974, along with Ohio Revised Code sections 5703.05, 5703.057, and 5747.08, governs the need for social security numbers on the form, highlighting its legal compliance requirements for tax administration. |

| Submission Information | Completed forms, along with necessary documentation, must be mailed to the Ohio Department of Taxation, specifically to the Income Tax Division – Ohio IT AR at P.O. Box 2476, Columbus, OH 43216-2476. |

Once you have completed your Ohio income tax or school district income tax return, either form Ohio IT 1040 or SD 100, the next step in ensuring that any due refund is properly requested is to complete the Ohio IT AR form. This is a designated form for taxpayers seeking to request a refund from their state or school district income tax payments. Care and attention to detail are crucial as this process involves financial transactions and sensitive personal information. Following the correct steps can aid in a smoother processing of your refund request.

Accuracy and completeness are imperative when filing the Ohio IT AR form to request a refund. By ensuring that each step is carefully followed and that all the required information is provided, taxpayers can facilitate a timely and smooth processing of their refund request. Note that attaching additional documentation or explanations can further substantiate the claim, leading to an expedited review process. It is also important to retain copies of the submitted form and any correspondence for your records.

What is the Ohio IT AR form?

The Ohio IT AR form is a refund application for residents who have filed an Ohio income tax return or school district income tax return using forms Ohio IT 1040 or SD 100. It's used to request a refund of overpaid taxes, and it requires detailed information about the taxpayer, including Social Security Number (SSN), address, and the amount of refund being requested.

When can I file the Ohio IT AR form?

You can file the Ohio IT AR form only after you've already submitted your Ohio income tax or school district income tax returns. Ensuring that these returns have been filed is crucial as the IT AR form relies on information from those documents to process your refund request.

What information do I need to include with my Ohio IT AR form?

You will need to include your personal details (including SSN and contact information), the tax type (either Individual Income or School District Income), and a thorough calculation of your refund. This calculation involves your total tax withheld, estimated payments, any previous payments or refunds, and refundable credits. Additionally, you must state the reasons for your refund claim and may need to attach supplementary documentation.

How do I calculate the refund requested on the Ohio IT AR form?

To calculate your refund, you'll start by summing up various payments and credits, including tax withheld, estimated and extension payments, amounts paid with previous returns, and any refundable credits (for individual income tax). From this total, you'll subtract any refunds you've already requested to find your net payment. The refund requested is calculated by subtracting your total Ohio or school district tax liability from your net payments, with the option to exclude interest from this calculation.

Where do I mail the completed Ohio IT AR form?

After completing and reviewing the Ohio IT AR form for accuracy, and signing under penalty of perjury, you should mail the form along with all required documents to: Ohio Department of Taxation, Attn: Income Tax Division – Ohio IT AR, P.O. Box 2476, Columbus, OH 43216-2476.

Is providing my Social Security number mandatory when filing the Ohio IT AR form?

Yes, providing your Social Security number is mandatory when filing the Ohio IT AR form. The requirement comes from federal and state laws to enable tax administration by the Ohio Department of Taxation. This measure helps in processing your tax information securely and accurately.

Can I attach additional sheets or supporting documentation to my Ohio IT AR form?

Yes, you are allowed and even encouraged to attach additional sheets or supporting documentation if necessary to fully explain your refund claim. Clear and comprehensive information and documentation can facilitate the processing of your refund request.

When filling out the Ohio IT AR form, which is needed after filing an income tax or school district income tax return, people often make mistakes that can delay processing. Here are eight common errors:

Here are additional tips to avoid mistakes:

Avoiding these common pitfalls can help ensure the refund process is smooth and efficient.

When dealing with the Ohio IT AR form, several other documents often come into play to ensure a comprehensive approach to managing your tax affairs. These documents not only support the refund application but also provide a detailed account of an individual’s tax situation, making the process smoother and more straightforward for both the taxpayer and the tax authority.

Together, these forms create a detailed picture of an individual's tax obligations and contributions throughout the tax year. By providing accurate and complete information across these documents, taxpayers can ensure their refund application is processed efficiently, potentially leading to a successful refund from the Ohio Department of Taxation.

The IRS Form 1040, U.S. Individual Income Tax Return, shares notable similarities with the Ohio IT AR form, specifically in its purpose for filing income tax returns and requesting refunds. Both forms require taxpayers to report income, deductions, and credits to determine their tax liability and any overpayment that may be due back as a refund. Taxpayer identification, such as Social Security numbers for individuals and their spouses, as well as contact information, are mandatory on both forms to ensure accurate processing and communication.

Form 1040-ES, Estimated Tax for Individuals, is akin to the Ohio IT AR in that it involves planning for and calculating tax liabilities ahead of disbursements. While the Ohio IT AR reconciles taxes already paid with the taxpayer's actual liability to request a refund, Form 1040-ES is used to estimate and pay taxes on income not subject to withholding taxes. The similarity lies in the forward-thinking approach to tax liability; one form addresses overpayment, while the other prevents underpayment.

The State of California Form 540, California Resident Income Tax Return, parallels the Ohio IT AR form through its state-specific income tax reporting and refund claiming processes. Both forms are designed to comply with their respective state tax laws and require detailed taxpayer information, income breakdowns, and the calculation of taxes owed versus payments made. This ensures taxpayers in both states can accurately request refunds for overpaid taxes.

The IRS Form 4868, Application for Automatic Extension of Time To File U.S. Individual Income Tax Return, shares the foundational purpose of adjusting tax filing deadlines, much like parts of the Ohio IT AR dealing with adjustments in tax payments or refund claims. Though the Form 4868 specifically grants additional time to file, not to amend or claim a refund, it similarly accommodates taxpayers' needs for flexibility regarding their tax obligations based on personal circumstances.

Form W-2, Wage and Tax Statement, is closely related to the Ohio IT AR form in the context of tax withholding and refund calculations. The W-2 form provides essential information about the income earned and taxes withheld by an employer, which taxpayers need to accurately fill out the Ohio IT AR form when claiming a refund. Both documents play pivotal roles in reconciling the actual tax liability with amounts previously paid through withholding or estimated payments.

The IRS Schedule C, Profit or Loss From Business, intersects with the Ohio IT AR form concerning the reporting of income and potential impact on tax refunds. Self-employed individuals use Schedule C to report their business earnings and expenses, affecting their overall tax liability. When filing the Ohio IT AR, taxpayers who also submit Schedule C must account for this self-employment income in their refund calculation, demonstrating how different sources of income influence refund claims.

Form 1099-MISC, Miscellaneous Income, and the Ohio IT AR form are related through the tax implications of non-employment income. Taxpayers receiving income documented on a Form 1099-MISC, such as freelance income, rents, or royalties, would need to report this in their income calculations on the Ohio IT AR form if applicable. This shared focus on accurately reporting all types of taxable income ensures individuals' tax liabilities and refund requests are correctly calculated.

The IRS Form 8863, Education Credits (American Opportunity and Lifetime Learning Credits), and the Ohio IT AR form connect through their handling of tax credits. Form 8863 allows taxpayers to claim deductions based on education expenses, directly affecting the tax liability calculated on forms like the Ohio IT AR. By including these credits, taxpayers can accurately assess their refund eligibility, illustrating the broader financial planning aspects of tax filing and refund applications.

When you're filling out the Ohio IT AR form, there are several things you should do to ensure the process goes smoothly, and some pitfalls you'll want to avoid. Here's a list of dos and don'ts that can help guide you through the process.

By following these guidelines, you can help ensure that your Ohio IT AR form is filled out correctly and processed efficiently. Remember, the key to a smooth process is accuracy and completeness.

Understanding the intricacies of tax forms can be challenging, and the Ohio IT AR form is no exception. A number of misconceptions exist regarding its use and requirements. Addressing these misconceptions is crucial for ensuring taxpayers can file accurately and confidently.

Many believe that the Ohio IT AR form is used for an initial tax return filing. In reality, the form is specifically designed for individuals who are seeking a refund application after they have already filed an Ohio income tax return or school district income tax return (form Ohio IT 1040 or SD 100). It's an important distinction, ensuring the form is used correctly in the refund process.

There's a common misunderstanding that the Ohio IT AR form is universally applicable to all taxpayers. However, it's primarily intended for those who have discovered they are owed a refund due to overpayment or an adjustment in their tax assessment. It is not a one-size-fits-all solution for all tax-related inquiries or adjustments.

For married individuals filing jointly, there might be confusion about the necessity of including a spouse's information. The form requires the Social Security Number (SSN) and name of both the taxpayer and the spouse, emphasizing that providing complete information is critical when filing for a joint refund.

A number of filers might presume that the refund calculation on the Ohio IT AR form is automatic or only requires minimal input. However, it is essential to manually calculate the refund requested by referring to previous tax forms (Ohio IT 1040 or SD 100) and accurately completing the calculation section. This ensures the requested refund amount is correct and supported by proper documentation.

Some may believe that the Ohio IT AR form can be filed at their convenience after the original tax return. It’s important to understand that there are specific timelines and deadlines governed by tax law that dictate when a refund application can be submitted. Submit to these temporal guidelines is crucial to ensure the application is processed in a timely manner.

Addressing these misconceptions ensures taxpayers are better informed about the specifics of the Ohio IT AR form, promoting accuracy and efficiency in the refund process.

Filing out and using the Ohio IT AR form, which stands for the Individual and School District Income Tax Refund Application, involves a few important steps and considerations. Understanding these can ensure that the process goes smoothly and that applicants comply correctly with Ohio's tax laws.

Lastly, while the process may seem straightforward, paying close attention to each step and requirement will help ensure that your refund request is processed efficiently. Remember, the Ohio Department of Taxation is available to assist with any questions or clarifications you might need.

Ohio State Tax Forms - The form provides a structured method for calculating net amount due or overpayment.

Ohio Ifsac Grandfather Application - This application form is specific to the Ohio Fire Academy’s criteria for grandfathering older certifications.