Blank Ohio Mf 2 Template

Blank Ohio Mf 2 Template

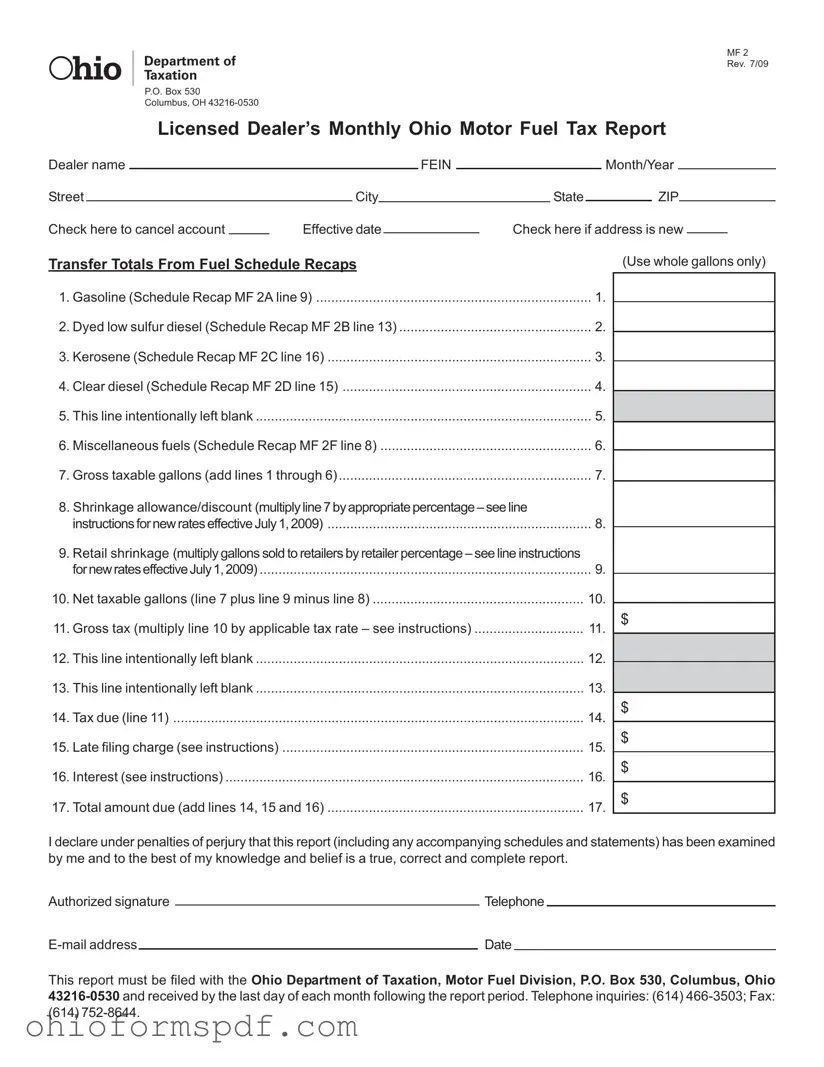

The Ohio Motor Fuel Tax Report, known as the Ohio MF 2 form, is a critical document for licensed dealers within the state, detailing their monthly fuel transactions subject to taxation. This comprehensive form issued by the Department of Taxation requires dealers to report on various types of fuels including gasoline, dyed low sulfur diesel, kerosene, and clear diesel, among others, to accurately calculate the gross taxable gallons. The form intricately breaks down these figures into net taxable gallons by taking into account allowances such as shrinkage and discounts for timely filings. Additionally, it outlines the tax rates applicable to different periods, emphasizing the importance of adherence to deadlines to avoid penalties like late filing charges and interest. The document emphasizes the necessity of accurate and timely submissions, underlining the legal requirement for dealers to declare this information under penalties of perjury. Furthermore, it meticulously guides users through the calculation of taxes due, while also providing avenues for contact and support from the Ohio Department of Taxation. As such, it plays a pivotal role in the administration of motor fuel taxes within Ohio, serving as a tool for both regulatory compliance and fiscal responsibility among fuel dealers.

HIO

HIO

MF 2

Department ofRev. 7/09

Taxation

P.O. Box 530

Columbus, OH

Licensed Dealer’s Monthly Ohio Motor Fuel Tax Report

Dealer name |

|

|

|

|

|

|

|

FEIN |

|

|

|

|

Month/Year |

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

Street |

|

|

|

|

City |

|

|

|

State |

|

|

ZIP |

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||

Check here to cancel account |

|

|

Effective date |

|

Check here if address is new |

|

|

|||||||||||||

Transfer Totals From Fuel Schedule Recaps |

|

|

|

|

(Use whole gallons only) |

|||||||||||||||

1. Gasoline (Schedule Recap MF 2A line 9) |

1. |

|

|

|

|

|

|

|||||||||||||

2. Dyed low sulfur diesel (Schedule Recap MF 2B line 13) |

2. |

|

|

|

|

|

|

|||||||||||||

3. Kerosene (Schedule Recap MF 2C line 16) |

3. |

|

|

|

|

|

|

|||||||||||||

4. Clear diesel (Schedule Recap MF 2D line 15) |

4. |

|

|

|

|

|

|

|||||||||||||

5. This line intentionally left blank |

|

|

|

|

|

5. |

|

|

|

|

|

|

||||||||

6. Miscellaneous fuels (Schedule Recap MF 2F line 8) |

6. |

|

|

|

|

|

|

|||||||||||||

7. Gross taxable gallons (add lines 1 through 6) |

7. |

|

|

|

|

|

|

|||||||||||||

8. Shrinkage allowance/discount |

|

|

|

|

|

|

||||||||||||||

instructionsfornewrateseffectiveJuly1,2009) |

8. |

|

|

|

|

|

|

|||||||||||||

|

|

|

|

|

|

|||||||||||||||

9. Retail shrinkage (multiply gallons sold to retailers by retailer percentage – see line instructions |

|

|

|

|

|

|

||||||||||||||

fornewrateseffectiveJuly1,2009) |

|

|

|

|

|

9. |

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

||||||||||

10. Net taxable gallons (line 7 plus line 9 minus line 8) |

10. |

|

|

|

|

|

|

|||||||||||||

$ |

|

|

|

|

|

|||||||||||||||

11. Gross tax (multiply line 10 by applicable tax rate – see instructions) |

11. |

|

|

|

|

|

||||||||||||||

12. This line intentionally left blank |

|

|

|

|

|

12. |

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

||||||||||

13. This line intentionally left blank |

|

|

|

|

|

13. |

|

|

|

|

|

|

||||||||

14. Tax due (line 11) |

|

|

|

|

|

14. |

$ |

|

|

|

|

|

||||||||

|

|

|

|

|

$ |

|

|

|

|

|

||||||||||

15. Late filing charge (see instructions) |

................................................................................ |

|

|

|

|

15. |

|

|

|

|

|

|||||||||

16. Interest (see instructions) |

|

|

|

|

|

16. |

$ |

|

|

|

|

|

||||||||

17. Total amount due (add lines 14, 15 and 16) |

17. |

$ |

|

|

|

|

|

|||||||||||||

I declare under penalties of perjury that this report (including any accompanying schedules and statements) has been examined by me and to the best of my knowledge and belief is a true, correct and complete report.

Authorized signature |

|

Telephone |

|

|

||

|

|

|||||

|

|

Date |

|

|

|

|

This report must be filed with the Ohio Department of Taxation, Motor Fuel Division, P.O. Box 530, Columbus, Ohio

|

|

MF 2 |

|

|

Rev. 7/09 |

|

|

Page 2 |

|

Return Instructions |

|

Line 8 |

Shrinkage – If your tax report is filed and timely paid, multiply the taxable gallons on line 7 by the appropriate |

|

|

shrinkage percentage. You are not entitled to the shrinkage allowance if your report is filed and/or paid after the |

|

|

due date. |

|

|

Reporting Period |

Shrinkage Percentage |

|

July 1, 1993 to June 30, 2005 |

3% (.03) |

|

July 1, 2005 to June 30, 2006 |

2.5% (.025) |

|

July 1, 2006 to June 30, 2007 |

1.95% (.0195) |

|

July 1, 2007 to June 30, 2009 |

1.90% (.019) – shrinkage and collection/administration discount |

|

Beginning July 1, 2009 to June 30, 2011 |

1.0% (.010) |

Line 9 |

Retail shrinkage – You must add back a percentage of all gallons of fuel sold to a retail dealers as defined in |

|

|

Ohio Revised Code Section 5735.01(O). Do not include gallons sold to retail dealers licensed under your FEIN. |

|

|

Reporting Period |

Shrinkage Percentage |

|

July 1, 1993 to June 30, 2005 |

1% (.01) |

|

July 1, 2005 to June 30, 2006 |

0.83% (.0083) |

|

July 1, 2006 to June 30, 2007 |

0.65% (.0065) |

|

July 1, 2007 to June 30, 2011 |

0.50% (.0050) |

Line 11 |

Tax rate |

|

|

Reporting Period |

Tax Rate Per Gallon |

|

July 1, 2003 to June 30, 2004 |

$0.24 |

|

July 1, 2004 to June 30, 2005 |

$0.26 |

|

Beginning July 1, 2005 |

$0.28 |

Lines 15/16 According to R.C. 5735.06(C), the tax report must be filed/received with the tax payment shown on the report, unless required to be submitted by EFT, by the due date. If the tax report and tax payment are not filed/received on or before the due date, you are liable for a “late filing charge” (line 15) and subject to interest (line 16) in addition to disallowance of any shrinkage claim. The late filing charge is the greater of 10% of your liability (line

14)or $50. The interest is to be calculated from the date the payment was due until the date the payment was actually received by the Ohio Treasurer of State or the Department of Taxation. The interest rate is determined on a calendar year basis and can change from year to year. Please visit our Web site at tax.ohio.gov for the current interest rate.

| Fact | Detail |

|---|---|

| Governing Law for Shrinkage and Retail Shrinkage Adjustments | Ohio Revised Code Section 5735.01(O) specifies how shrinkage and retail shrinkage adjustments are calculated for motor fuel tax reports. |

| Submission Address | The form must be filed with the Ohio Department of Taxation, Motor Fuel Division, P.O. Box 530, Columbus, Ohio 43216-0530. |

| Submission Deadline | Reports are due by the last day of each month following the report period. |

| Contact Information | Telephone inquiries can be made at (614) 466-3503; Fax: (614) 752-8644. |

| Penalty for Late Filing | Per R.C. 5735.06(C), late filings are subject to a charge (the greater of 10% of liability or $50) and interest from the due date to the received date. |

| Shrinkage Allowance Rates | Shrinkage allowance rates have varied over time, with a decrease from 3% before July 2005 to 1% starting July 2009. |

| Tax Rate Changes Over Time | The motor fuel tax rate has increased from $0.24 per gallon before July 2004 to $0.28 per gallon starting July 2005. |

The Ohio Mf 2 form is an essential document that licensed dealers must submit monthly for reporting motor fuel taxes. It's a comprehensive form that requests information on various types of fuel transactions and calculates the gross taxable gallons, net taxable gallons, and tax due. Timely and accurate completion of this report ensures compliance with state taxation regulations, avoiding any penalties or late fees. The instructions below will guide the applicant through the step-by-step process to fill out the form correctly. It's crucial to follow these steps carefully and review the report thoroughly before submission.

After filling out the form, verify all the information for completeness and accuracy. This report must be filed with the Ohio Department of Taxation, Motor Fuel Division by the last day of the month following the report period. Ensure that the form along with any necessary payments are submitted on time to avoid potential penalties. If you have any inquiries or require assistance, contact the provided telephone number or visit the official website.

What is the purpose of the Ohio MF 2 Form?

The Ohio MF 2 Form, known as the Licensed Dealer's Monthly Ohio Motor Fuel Tax Report, is a document designed for licensed fuel dealers within the state of Ohio. Its primary purpose is to report and calculate the taxes owed on the motor fuel (like gasoline, diesel, and kerosene) that these dealers have distributed over the month. This comprehensive reporting ensures that the state can accurately collect taxes on fuel distribution, which, in turn, contributes to state-funded projects and services. Dealers need to provide detailed information, including total gallons of each type of fuel sold, adjustments for shrinkage, and calculate the total tax due. Timely and accurate completion of this form ensures compliance with Ohio tax laws and helps maintain the infrastructure funded by these taxes.

How do I calculate shrinkage on the Ohio MF 2 Form?

Calculating shrinkage on the Ohio MF 2 Form involves applying specific percentages to your total taxable gallons. Shrinkage accounts for fuel loss due to factors like evaporation and spillage. Two types of shrinkage are considered: general shrinkage and retail shrinkage. For general shrinkage, you multiply the gross taxable gallons by the current shrinkage percentage for your reporting period. Retail shrinkage adjustments involve adding back a percentage of all gallons sold to retail dealers, as defined by specific guidelines. Each type of shrinkage has its own rate, which has changed over the years. It's crucial to refer to the instructions for the form to apply the correct percentages for your reporting period. Importantly, you can only claim shrinkage allowances if your report and payment are filed by the due date.

What happens if I file the Ohio MF 2 Form late?

Filing the Ohio MF 2 Form late can have multiple consequences. Firstly, you will lose the entitlement to claim a shrinkage allowance, directly affecting the amount of tax you are liable for by increasing it. Besides this immediate impact, you will also be subject to a late filing charge and interest on the tax due. The late filing charge is calculated as the greater of 10% of your tax liability (as shown on line 14 of the form) or $50. Additionally, interest accrues from the due date until the Ohio Treasurer of State or the Department of Taxation receives the payment. The interest rate is subject to change annually, so you should check the current rate if you find yourself in this situation. Compliance with filing deadlines is, therefore, essential to avoid unnecessary penalties and interest charges.

Where and when should the Ohio MF 2 Form be submitted?

The Ohio MF 2 Form must be submitted to the Ohio Department of Taxation, Motor Fuel Division, at the address provided on the form: P.O. Box 530, Columbus, Ohio 43216-0530. Importantly, the submission, along with any tax payment due, must be received by the last day of each month following the report period to avoid penalties for late submission. This strict deadline ensures that the tax collection process is efficient and timely. For dealers who are required or opt to submit payments electronically, specific instructions regarding electronic funds transfer (EFT) must be followed. Keeping abreast of due dates and ensuring proper submission methods are crucial for compliance and for avoiding unnecessary late fees and interest charges.

When filling out the Ohio MF 2 form, licensed dealers can inadvertently make several mistakes that may affect the accuracy of their monthly motor fuel tax report. Below is a curated list of the common oversights and errors, along with an explanation for each:

Being aware of these mistakes can guide licensed dealers through a more accurate and compliant process of reporting their monthly motor fuel tax activities to the Ohio Department of Taxation. Ensuring accuracy in each section of the Ohio MF 2 form not only upholds tax compliance but also prevents potential penalties associated with reporting errors.

When dealing with the Ohio Mf 2 form, a Licensed Dealer’s Monthly Ohio Motor Fuel Tax Report, it's frequently just one piece of the broader compliance and reporting puzzle for those in the motor fuel industry within Ohio. This essential form, filled out by licensed dealers to account for the motor fuel tax owed based on gallons sold, is often submitted along with various other documents and forms. Understanding these accompanying documents can streamline the tax reporting process and ensure compliance with state requirements.

Each of these documents plays a pivotal role in the tax administration process for motor fuels in Ohio. They not only facilitate the accurate and timely reporting and payment of motor fuel taxes but also help maintain the integrity and legality of the fuel distribution network. For businesses engaged in the selling of motor fuel, understanding and correctly using these forms is crucial to operating successfully within Ohio's regulatory framework.

The Ohio MF 2 form closely resembles the State Sales Tax Report, as both require detailed accounting of transactions within a specific period. Similar to how the Ohio MF 2 form demands precise reporting of motor fuel transactions and calculations based on specific tax rates and allowed deductions like shrinkage, the State Sales Tax Report mandates businesses to meticulously document their sales transactions, apply the correct sales tax rate, and calculate the total tax owing. Both forms play a critical role in ensuring compliance with state regulations and contribute to the financial infrastructure by providing necessary revenue.

Another document akin to the Ohio MF 2 form is the Federal Excise Tax Return, which also revolves around the principle of taxing specific goods, albeit at a federal level. The Federal Excise Tax Return, much like the Ohio MF 2 form, involves the reporting of taxes on particular items – in this case, the focus is on goods like gasoline, alcohol, and tobacco. Both documents require registrants to accurately report quantities and calculate taxes based on prescribed rates, although the Federal Excise Tax Return applies to a broader scope of products and is regulated at a national level.

The Ohio Commercial Activity Tax (CAT) Return shares similarities with the Ohio MF 2 form in that both target businesses operating within Ohio and require detailed reporting of specific types of activities. The CAT return focuses on the privilege of doing business in Ohio, requiring companies to report gross receipts and calculate the tax due. Although targeting different aspects of business operations, both forms ensure businesses contribute their fair share to the state's economic structure, based on their operational scope.

The Unemployment Insurance Tax Return, while primarily concerned with workforce-related taxes, also shares a functional similarity with the Ohio MF 2 form. Employers are required to report wages and calculate taxes owed for unemployment insurance, just as the Ohio MF 2 form mandates the detailed reporting and tax calculation based on motor fuel transactions. Both are essential for the provision of governmental services, either by supporting unemployed workers or by funding infrastructure through fuel taxes.

The Inventory Tax Statement, prevalent in some states, requires businesses to report the value of their inventory and calculate a tax based on this valuation. This bears resemblance to the Ohio MF 2 form’s requirement for fuel dealers to report volumes of different fuel types and compute the tax based. While one focuses on the valuation of tangible goods and the other on volumetric transactions, both forms serve as instruments for tax collection based on business assets.

The Hazardous Waste Tax Return is another document with objectives comparable to the Ohio MF 2 form, focusing on the environmental aspect. Companies dealing with hazardous waste must report quantities and pay taxes accordingly, similar to how fuel dealers must account for fuel transactions. Both forms aim to mitigate the environmental impact of commercial activities by imposing taxes to fund respective state environmental protection initiatives.

The Alcohol Beverage Tax Return, like the Ohio MF 2 form, targets a specific product category and requires businesses to report on transactions related to this category. Alcohol distributors must provide detailed accounts of their sales and calculate taxes due, akin to fuel dealers' responsibilities under the Ohio MF 2 form. These documents ensure that taxes levied on highly regulated goods are accurately reported and collected, reflecting the government’s oversight on specific industries.

Lastly, the Tobacco Product Tax Return similarly parallels the Ohio MF 2 form by focusing on a specialized sector. Tobacco distributors are required to report sales and inventory changes and calculate the taxes due on these products. Both forms are critical in regulating industries with significant health and environmental considerations, enforcing detailed reporting and taxation to manage the impact of these businesses on society and the economy.

When preparing and submitting the Ohio MF 2 form, which serves as the Licensed Dealer’s Monthly Ohio Motor Fuel Tax Report, it is important to adhere to specific guidelines to ensure the form is filled out correctly and completely. The following are recommendations on what should and shouldn’t be done during this process:

Do:

Don't:

Understanding the Ohio MF 2 form and its specifics can be complex, leading to various misconceptions. Here are seven common misunderstandings explained to help clarify their complexities:

Misconception 1: The Ohio MF 2 form is only for gasoline dealers. The form actually covers various types of fuel, including dyed low sulfur diesel, kerosene, clear diesel, and miscellaneous fuels, not just gasoline. This is evident from the different schedules like MF 2A, MF 2B, etc., which are designated for different fuel types.

Misconception 2: All lines need to be filled. The form itself has lines that are intentionally left blank, such as lines 5, 12, and 13. These are not to be filled by the dealer; they are designed that way to ensure clarity and avoid confusion in the reporting process.

Misconception 3: Shrinkage is automatically calculated for all types of fuel. Shrinkage allowance or discount is specific and can only be applied to gross taxable gallons under certain conditions, which are clearly stated in the return instructions. Shrinkage rates have changed over time and are not a one-size-fits-all percentage.

Misconception 4: The form is complicated and requires a tax professional to fill it out. While it’s always wise to consult with a professional if you’re unsure, the Ohio MF 2 form comes with detailed instructions that, when followed carefully, allow most dealers to fill it out correctly on their own.

Misconception 5: The tax rate is static. The tax rate per gallon has changed over the years and can vary depending on legislative changes. It’s crucial to refer to the most current instructions or check the official Ohio Department of Taxation website for the applicable rates during your reporting period.

Misconception 6: You can only file the form via mail. Although the form provides a mailing address, the Ohio Department of Taxation has introduced electronic filing systems for many tax forms, including fuel tax reports. It's advisable to check the current filing options available.

Misconception 7: Late filing charges and interest are negotiable. The charges and interest rates applied to late filings are determined by state law and are not subject to negotiation. The late filing charge is the greater of 10% of the tax liability or $50, and interest is calculated from the due date to the payment date at the current rate.

Dispelling these misconceptions helps in understanding the Ohio MF 2 form better, ensuring accurate and timely reporting for licensed dealers. It’s always beneficial to review the official instructions provided with the form or consult with the Ohio Department of Taxation for any uncertainties.

Filling out and using the Ohio MF 2 form, a crucial tool for licensed dealers reporting motor fuel taxes, requires careful attention to detail and awareness of specific guidelines. Here are key takeaways to ensure compliance and accuracy:

By adhering to these guidelines, licensed dealers can confidently navigate the complexities of the Ohio MF 2 form, ensuring their motor fuel tax reporting is precise and compliant with state requirements.

Ohio 3 Q - Completion and submission of the Form 3-Q are integral steps in adhering to the statutory requirements set forth by Ohio securities law.

How Do I Find Out How Much I Owe the Ohio Attorney General - Addresses the need for a reliable, official source of payoff information directly from the Ohio Attorney General's office.

Ohio School Tax - If less tax was withheld than necessary, this form helps calculate the balance due for each school district.