Blank Ohio Sd 101 Template

Blank Ohio Sd 101 Template

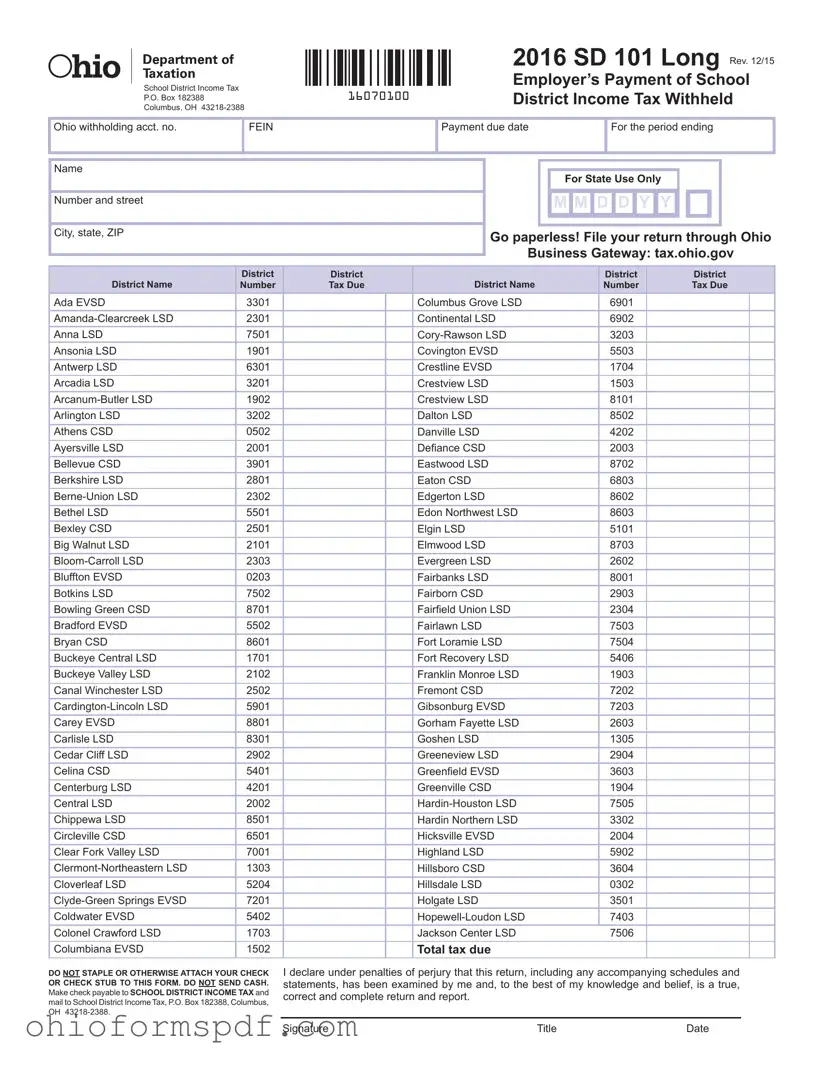

In the landscape of Ohio's tax obligations, the SD 101 form plays a crucial role for employers. This document, formally known as the School District Income Tax form, is a vessel through which employers remit taxes withheld from their employees' earnings to the state. The importance of this form cannot be overstated, as it ensures the proper funding of school districts throughout Ohio, directly impacting the quality of education and resources available to students. The form, which must be sent to the specified address in Columbus, Ohio, lists an extensive range of school districts, each with its distinct tax due, underscoring the tailored approach to local education funding. Employers are required to fill out their withholding account number, the period ending, and detailed tax due information for each relevant school district. Moreover, the form streamlines the process by urging filers to go paperless, thereby promoting efficiency and environmental consciousness. The precision and accuracy in completing the SD 101 form reflect not only compliance with state tax regulations but also a commitment to contributing to the educational development of Ohio's next generation.

School District Income Tax

P.O. Box 182388

Columbus, OH

2016 SD 101 Long Rev. 12/15

Employer’s Payment of School

16070100 |

District Income Tax Withheld |

|

Ohio withholding acct. no.

FEIN

Payment due date

For the period ending

Name

Number and street

City, state, ZIP

For State Use Only

M M D D Y Y |

Go paperless! File your return through Ohio

Business Gateway: tax.ohio.gov

|

District |

District |

|

District |

District |

||

District Name |

Number |

Tax Due |

District Name |

Number |

Tax Due |

||

Ada EVSD |

3301 |

|

|

Columbus Grove LSD |

6901 |

|

|

|

|

|

|

|

|

|

|

2301 |

|

|

Continental LSD |

6902 |

|

|

|

Anna LSD |

7501 |

|

|

3203 |

|

|

|

Ansonia LSD |

1901 |

|

|

Covington EVSD |

5503 |

|

|

|

|

|

|

|

|

|

|

Antwerp LSD |

6301 |

|

|

Crestline EVSD |

1704 |

|

|

|

|

|

|

|

|

|

|

Arcadia LSD |

3201 |

|

|

Crestview LSD |

1503 |

|

|

|

|

|

|

|

|

|

|

1902 |

|

|

Crestview LSD |

8101 |

|

|

|

|

|

|

|

|

|

|

|

Arlington LSD |

3202 |

|

|

Dalton LSD |

8502 |

|

|

|

|

|

|

|

|

|

|

Athens CSD |

0502 |

|

|

Danville LSD |

4202 |

|

|

|

|

|

|

|

|

|

|

Ayersville LSD |

2001 |

|

|

Defiance CSD |

2003 |

|

|

|

|

|

|

|

|

|

|

Bellevue CSD |

3901 |

|

|

Eastwood LSD |

8702 |

|

|

|

|

|

|

|

|

|

|

Berkshire LSD |

2801 |

|

|

Eaton CSD |

6803 |

|

|

|

|

|

|

|

|

|

|

2302 |

|

|

Edgerton LSD |

8602 |

|

|

|

|

|

|

|

|

|

|

|

Bethel LSD |

5501 |

|

|

Edon Northwest LSD |

8603 |

|

|

|

|

|

|

|

|

|

|

Bexley CSD |

2501 |

|

|

Elgin LSD |

5101 |

|

|

|

|

|

|

|

|

|

|

Big Walnut LSD |

2101 |

|

|

Elmwood LSD |

8703 |

|

|

|

|

|

|

|

|

|

|

2303 |

|

|

Evergreen LSD |

2602 |

|

|

|

|

|

|

|

|

|

|

|

Bluffton EVSD |

0203 |

|

|

Fairbanks LSD |

8001 |

|

|

|

|

|

|

|

|

|

|

Botkins LSD |

7502 |

|

|

Fairborn CSD |

2903 |

|

|

Bowling Green CSD |

8701 |

|

|

Fairfi eld Union LSD |

2304 |

|

|

Bradford EVSD |

5502 |

|

|

Fairlawn LSD |

7503 |

|

|

|

|

|

|

|

|

|

|

Bryan CSD |

8601 |

|

|

Fort Loramie LSD |

7504 |

|

|

|

|

|

|

|

|

|

|

Buckeye Central LSD |

1701 |

|

|

Fort Recovery LSD |

5406 |

|

|

|

|

|

|

|

|

|

|

Buckeye Valley LSD |

2102 |

|

|

Franklin Monroe LSD |

1903 |

|

|

|

|

|

|

|

|

|

|

Canal Winchester LSD |

2502 |

|

|

Fremont CSD |

7202 |

|

|

|

|

|

|

|

|

|

|

5901 |

|

|

Gibsonburg EVSD |

7203 |

|

|

|

|

|

|

|

|

|

|

|

Carey EVSD |

8801 |

|

|

Gorham Fayette LSD |

2603 |

|

|

|

|

|

|

|

|

|

|

Carlisle LSD |

8301 |

|

|

Goshen LSD |

1305 |

|

|

|

|

|

|

|

|

|

|

Cedar Cliff LSD |

2902 |

|

|

Greeneview LSD |

2904 |

|

|

|

|

|

|

|

|

|

|

Celina CSD |

5401 |

|

|

Greenfield EVSD |

3603 |

|

|

|

|

|

|

|

|

|

|

Centerburg LSD |

4201 |

|

|

Greenville CSD |

1904 |

|

|

|

|

|

|

|

|

|

|

Central LSD |

2002 |

|

|

7505 |

|

|

|

|

|

|

|

|

|

|

|

Chippewa LSD |

8501 |

|

|

Hardin Northern LSD |

3302 |

|

|

|

|

|

|

|

|

|

|

Circleville CSD |

6501 |

|

|

Hicksville EVSD |

2004 |

|

|

|

|

|

|

|

|

|

|

Clear Fork Valley LSD |

7001 |

|

|

Highland LSD |

5902 |

|

|

1303 |

|

|

Hillsboro CSD |

3604 |

|

|

|

|

|

|

|

|

|

|

|

Cloverleaf LSD |

5204 |

|

|

Hillsdale LSD |

0302 |

|

|

|

|

|

|

|

|

|

|

7201 |

|

|

Holgate LSD |

3501 |

|

|

|

Coldwater EVSD |

5402 |

|

|

7403 |

|

|

|

|

|

|

|

|

|

|

|

Colonel Crawford LSD |

1703 |

|

|

Jackson Center LSD |

7506 |

|

|

|

|

|

|

|

|

|

|

Columbiana EVSD |

1502 |

|

|

Total tax due |

|

|

|

DO NOT STAPLE OR OTHERWISE ATTACH YOUR CHECK OR CHECK STUB TO THIS FORM. DO NOT SEND CASH. Make check payable to SCHOOL DISTRICT INCOME TAX and mail to School District Income Tax, P.O. Box 182388, Columbus, OH

I declare under penalties of perjury that this return, including any accompanying schedules and statements, has been examined by me and, to the best of my knowledge and belief, is a true, correct and complete return and report.

Signature |

Title |

Date |

For the Period Ending

Ohio Withholding Account No.

16070200

SD 101 Long

Rev. 12/15

Page 2

|

District |

District |

|

|

District |

District |

|

District Name |

Number |

Tax Due |

|

District Name |

Number |

Tax Due |

|

Jefferson LSD |

4901 |

|

|

Parkway LSD |

5405 |

|

|

Jennings LSD |

6903 |

|

|

Patrick Henry LSD |

3504 |

|

|

4503 |

|

|

Paulding EVSD |

6302 |

|

|

|

|

|

|

|

|

|

|

|

Jonathan Alder LSD |

4902 |

|

|

Perrysburg EVSD |

8708 |

|

|

Kalida LSD |

6904 |

|

|

Pettisville LSD |

2604 |

|

|

Kenton CSD |

3303 |

|

|

Pickerington LSD |

2307 |

|

|

Lakota LSD |

7204 |

|

|

Piqua CSD |

5507 |

|

|

|

|

|

|

|

|

|

|

Lancaster CSD |

2305 |

|

|

7007 |

|

|

|

|

|

|

|

|

|

|

|

Leipsic LSD |

6905 |

|

|

Preble Shawnee LSD |

6804 |

|

|

3205 |

|

|

Reynoldsburg CSD |

2509 |

|

|

|

Liberty Center LSD |

3502 |

|

|

Ridgemont LSD |

3304 |

|

|

Liberty |

2306 |

|

|

Riverdale LSD |

3305 |

|

|

Licking Valley LSD |

4506 |

|

|

Riverside LSD |

4604 |

|

|

Logan Elm LSD |

6502 |

|

|

Ross LSD |

0908 |

|

|

London CSD |

4903 |

|

|

Russia LSD |

7507 |

|

|

0303 |

|

|

Sebring LSD |

5008 |

|

|

|

Madison LSD |

0905 |

|

|

Seneca East LSD |

7406 |

|

|

McComb LSD |

3206 |

|

|

Shelby CSD |

7008 |

|

|

Mechanicsburg EVSD |

1102 |

|

|

South Central LSD |

3905 |

|

|

Miami East LSD |

5504 |

|

|

Southeastern LSD |

1205 |

|

|

8604 |

|

|

Southwest LSD |

3118 |

|

|

|

|

|

|

|

|

|

|

|

Miller |

6906 |

|

|

Southwest Licking LSD |

4510 |

|

|

|

|

|

|

|

|

|

|

5505 |

|

|

Spencerville LSD |

0209 |

|

|

|

|

|

|

|

|

|

|

|

Minster LSD |

0601 |

|

|

Springfield LSD |

5010 |

|

|

|

|

|

|

|

|

|

|

Mississinawa Valley LSD |

1905 |

|

|

Stryker LSD |

8607 |

|

|

Mohawk LSD |

8802 |

|

|

Swanton LSD |

2606 |

|

|

Monroeville LSD |

3902 |

|

|

Talawanda CSD |

0909 |

|

|

Montpelier EVSD |

8605 |

|

|

Teays Valley LSD |

6503 |

|

|

|

|

|

|

|

|

|

|

Mount Gilead EVSD |

5903 |

|

|

Triad LSD |

1103 |

|

|

National Trail LSD |

6802 |

|

|

6806 |

|

|

|

New Bremen LSD |

0602 |

|

|

1906 |

|

|

|

|

|

|

|

|

|

|

|

New Knoxville LSD |

0603 |

|

|

Triway LSD |

8509 |

|

|

New Lebanon LSD |

5708 |

|

|

Troy CSD |

5509 |

|

|

New London LSD |

3903 |

|

|

Twin Valley Community LSD |

6805 |

|

|

|

|

|

|

|

|

|

|

New Miami LSD |

0907 |

|

|

7106 |

|

|

|

|

|

|

|

|

|

|

|

New Riegel LSD |

7404 |

|

|

United LSD |

1510 |

|

|

|

|

|

|

|

|

|

|

Newark CSD |

4507 |

|

|

Upper Sandusky EVSD |

8803 |

|

|

|

|

|

|

|

|

|

|

Newton LSD |

5506 |

|

|

Upper Scioto Valley LSD |

3306 |

|

|

|

|

|

|

|

|

|

|

North Baltimore LSD |

8705 |

|

|

Valley View LSD |

5713 |

|

|

|

|

|

|

|

|

|

|

North Fork LSD |

4508 |

|

|

Van Wert CSD |

8104 |

|

|

North Union LSD |

8003 |

|

|

Vanlue LSD |

3208 |

|

|

Northeastern LSD |

1203 |

|

|

Versailles EVSD |

1907 |

|

|

|

|

|

|

|

|

|

|

Northmor LSD |

5904 |

|

|

Walnut Township LSD |

2308 |

|

|

Northwest LSD |

7612 |

|

|

Wapakoneta CSD |

0605 |

|

|

Northwestern LSD |

1204 |

|

|

Wayne Trace LSD |

6303 |

|

|

Northwestern LSD |

8505 |

|

|

Waynesfi |

0606 |

|

|

Northwood LSD |

8706 |

|

|

Wellington EVSD |

4715 |

|

|

Norwalk CSD |

3904 |

|

|

West |

1105 |

|

|

Norwayne LSD |

8504 |

|

|

Western Reserve LSD |

3906 |

|

|

Oberlin CSD |

4712 |

|

|

Willard CSD |

3907 |

|

|

Old Fort LSD |

7405 |

|

|

Wilmington CSD |

1404 |

|

|

Otsego LSD |

8707 |

|

|

Wyoming CSD |

3122 |

|

|

|

|

|

|

|

|

|

|

6907 |

|

|

Xenia Community CSD |

2906 |

|

|

|

Ottoville LSD |

6908 |

|

|

Yellow Springs EVSD |

2907 |

|

|

6909 |

|

|

Zane Trace LSD |

7107 |

|

|

|

|

|

|

|

|

|

|

|

| Fact | Description |

|---|---|

| Purpose | This form is used for the payment of School District Income Tax Withheld in Ohio. |

| Mailing Address | Payments and forms are to be sent to School District Income Tax, P.O. Box 182388, Columbus, OH 43218-2388. |

| Payment Due Date | Specific due dates for payment are noted on the form, corresponding to the period ending dates for the tax withheld. |

| Governing Law | The tax collection and enforcement are governed by Ohio state laws regulating school district income taxes. |

Filing Ohio's SD 101 form correctly is crucial for employers to ensure that school district income tax withholdings are accurately reported and paid. This process involves providing detailed information about the employer, including the withholding account number and specific amounts withheld for each school district. To clarify, these steps break down how to complete the form from start to finish, ensuring compliance and timely payment. It's important for employers to pay close attention to each section to avoid errors that could lead to penalties or additional scrutiny.

Upon successful completion and submission of the SD 101 form, along with the appropriate payment, employers have taken the necessary steps to comply with Ohio's school district income tax withholding requirements. It's essential to keep a copy of the filed form and the payment confirmation for record-keeping purposes. Timely and accurate filing helps prevent potential issues with the Ohio Department of Taxation and ensures that school districts receive the funding needed from tax withholdings.

What is the Ohio SD 101 form?

The Ohio SD 101 form is a document used by employers to report and pay school district income taxes withheld from employees' wages. This is specifically for employers in the state of Ohio who have withheld taxes for one or more school districts.

Where does one mail the completed Ohio SD 101 form?

The completed form should be mailed to the School District Income Tax, P.O. Box 182388, Columbus, OH 43218-2388. It is important to ensure that the form is filled out correctly and completely to avoid processing delays.

Can the Ohio SD 101 form be filed electronically?

Yes, the form can be filed electronically through the Ohio Business Gateway at tax.ohio.gov. This paperless option provides a more convenient and faster way for employers to file their return and payment.

When is the Ohio SD 101 form due?

The due date for the Ohio SD 101 form varies based on the reporting period. Employers should refer to the instructions on their specific form or consult the Ohio Department of Taxation's website for more information on filing deadlines.

What information is required on the Ohio SD 101 form?

The form requires detailed information including the employer's Ohio withholding account number, Federal Employer Identification Number (FEIN), the period ending date, the name and address of the employer, a detailed list of school districts with the corresponding taxes due, and the total tax due. A signature, title, and date are also required at the bottom of the form to certify the accuracy of the information provided.

Is it necessary to attach the payment check to the Ohio SD 101 form?

No, employers should not staple or otherwise attach their payment check or check stub to the form. This helps in processing the payments more efficiently. Checks should be made payable to SCHOOL DISTRICT INCOME TAX.

What should one do if they need to amend an already filed Ohio SD 101 form?

If an employer discovers an error on a previously filed SD 101 form, they should consult the Ohio Department of Taxation's guidelines on amending returns. In many cases, a corrected form can be submitted to report the accurate information.

Who can I contact for more information or assistance with the Ohio SD 101 form?

For more information or assistance, employers can contact the Ohio Department of Taxation directly through their website at tax.oh every 'io.gov' or by phone. They offer guidance and support for any queries related to the SD 101 form and its filing requirements.

Filling out the Ohio SD 101 form, which pertains to the Employer’s Payment of School District Income Tax Withheld, is a crucial task that demands accuracy to ensure the proper processing of tax payments. Mistakes can lead to unnecessary delays or issues with tax submissions. Outlined below are four common errors identified in the completion of this form:

Selecting the Incorrect School District Number: Each school district in Ohio has a unique identifying number. One of the frequent mistakes is selecting or entering the wrong district number on the form. This error can route the funds to the incorrect district, complicating the tax payment process for both the employer and the tax authorities.

Inaccurate Tax Due Calculation: Accurately calculating the tax due is vital. Errors in calculation can occur due to misunderstanding the tax rates applicable to the respective school district or incorrect assessment of taxable income. Such mistakes can lead to underpayment or overpayment of taxes.

Omitting Employer Identification Number (EIN) or Ohio Withholding Account Number: The form requires both the Federal Employer Identification Number (FEIN) and the Ohio Withholding Account Number. Failure to provide this information can prevent the Ohio Department of Taxation from properly attributing the tax payment to the right employer, leading to discrepancies in tax records.

Failure to Sign the Document: An often overlooked but critical step is the requirement for the form to be signed by an authorized individual. A missing signature can render the submission invalid, as it signifies the attestation of the document's accuracy and completeness under penalties of perjury.

Ensuring the careful review and accurate completion of the Ohio SD 101 form is imperative for the timely and correct processing of school district income tax payments. Attention to detail can prevent the common mistakes detailed above, facilitating a smoother transaction with tax authorities.

Completing the Ohio SD 101 Long Form, significant for the payment of school district income tax withheld by employers, often necessitates gathering and preparing several other forms and documents to ensure accuracy and compliance. These documents provide essential information regarding the business's financial obligations to the state and its employees. Below is a list of forms and documents commonly used in conjunction with the Ohio SD 101 Form:

Each of these documents plays a vital role in ensuring the accuracy and compliance of the Ohio SD 101 Long Form submission. They not only facilitate the proper calculation of the school district tax owed but also help maintain an organized record of payroll and tax payments throughout the fiscal year. Ensuring these documents are accurately completed and maintained will significantly ease the process of adhering to state tax obligations.

The Ohio SD 101 form shares similarities with the Form 941, which is the Employer's Quarterly Federal Tax Return. Both documents are crucial for reporting taxes withheld from employees' wages. The SD 101 form specifically deals with the school district income tax withheld in Ohio, while Form 941 focuses on federal income tax, social security, and Medicare taxes. They are alike in that they both require employers to report tax withholdings and provide a breakdown of the tax due for a specific period.

Similar to the Ohio SD 101, the W-2 form, or Wage and Tax Statement, is essential for reporting an employee's annual wages and the amount of taxes withheld from their paycheck. While the W-2 form is sent directly to employees for their personal tax filings and to the Social Security Administration, the SD 101 form is submitted to the Ohio Department of Taxation. Both forms play a key role in tax compliance and ensure the accurate reporting of withheld taxes.

The State Unemployment Tax Act (SUTA) tax reporting form is another document sharing common ground with the Ohio SD 101 form. Both forms involve payments related to employment but focus on different areas: the SD 101 form addresses school district income tax withholdings, while SUTA focuses on unemployment tax contributions to the state. Employers are responsible for submitting both forms to the respective state authorities to fulfill legal tax obligations.

Ohio's IT 3 form, or Transmittal of Wage and Tax Statements, also parallels the Ohio SD 101 in functionality. This form is used to summarize and transmit employee W-2s and/or 1099s to the state tax department. Like the SD 101, the IT 3 form is part of the process of reporting taxes withheld from employees, albeit for different tax types and purposes. Each form ensures that the state receives accurate information on taxes withheld from wages.

The Employer's Annual Federal Unemployment (FUTA) Tax Return, or Form 940, resembles the Ohio SD 101 form in its purpose of reporting taxes related to employment. While Form 940 reports the employer’s annual federal unemployment tax liability, the SD 101 form focuses on school district income tax withholdings. Both documents are key to fulfilling federal and state tax obligations, respectively.

Form 1099, particularly the 1099-MISC, is often used to report payments to non-employees. This form has a similarity with the Ohio SD 101 in that both involve reporting financial information relevant to tax obligations. However, while the 1099-MISC focuses on miscellaneous income paid to individuals, the SD 101 form is focused on the school district income tax withheld from employees' wages.

The Quarterly Federal Excise Tax Return, or Form 720, is used to report and pay the federal excise taxes, presenting another parallel to the Ohio SD 101 form. Though they target different tax types—excise versus school district income tax—their role in tax collection and reporting within the framework of employment is crucial. Both forms require detailed record-keeping and adherence to deadlines to ensure compliance.

The Ohio Commercial Activity Tax (CAT) return, which businesses operating in Ohio must file, serves a purpose similar to that of the Ohio SD 101 in the broader context of tax reporting. While the CAT return deals with the tax on gross receipts for business conducted within the state, the SD 101 encompasses employee school district income tax withholdings. Each form contributes to the comprehensive tax landscape businesses must navigate.

Finally, the Form 1040, U.S. Individual Income Tax Return, shares the ultimate goal of tax reporting with the Ohio SD 101 form, albeit from the perspective of individual taxpayers rather than employers. While individuals use Form 1040 to report their annual income and calculate federal tax liability, the SD 101 form allows employers to report and pay withheld school district income taxes. Both are integral to the financing of government services and education.

When filling out the Ohio SD 101 form, which is used for the employer’s payment of school district income tax withheld, several best practices should be followed to ensure accuracy and compliance with tax regulations. Carefully adhering to these dos and don’ts can streamline the process, avoiding common errors and potential penalties.

Do:By meticulously following these guidelines, employers can effectively manage their responsibilities in reporting and paying school district income taxes in Ohio, thereby contributing to the support of their local education systems.

There are several misconceptions about the Ohio SD 101 form, which is crucial for employers to understand for accurate tax reporting and compliance. Exploring these misconceptions can clarify the reporting process and ensure that taxes are filed correctly and efficiently.

It’s Only for Large Employers: Many believe the Ohio SD 101 form is exclusively for large businesses. In reality, any employer who withholds school district income tax from employees' wages must file this form, regardless of the business size.

Only Ohio-based Companies Need to File: Another common misconception is that only businesses located within Ohio need to file the SD 101 form. However, any employer with employees subject to Ohio school district income tax must file, irrespective of the company's location.

Filing Is Annual: Some may think that the Ohio SD 101 is filed annually. The truth is that employers are generally required to file this form quarterly to report and pay the withheld taxes timely.

Electronic Filing Is Optional: With the emphasis on traditional paper filing systems, it's often misunderstood that electronic filing is just an option. The state encourages electronic filing through the Ohio Business Gateway for efficiency and security, making it preferable in many instances.

Payments Can Be Attached to the Form: A key point of confusion is around how to submit payments. The instructions specifically state not to staple or otherwise attach the payment to the SD 101 form, countering the common practice for other forms.

Only Checks Are Accepted for Payment: While checks are commonly used, they are not the only form of payment accepted. Employers can also make payments electronically, offering flexibility and security in the transaction process.

All School Districts Have the Same Tax Rate: Employers often mistakenly believe that one tax rate applies to all Ohio school districts. Each district may have a different tax rate, necessitating careful review to ensure accurate withholding and reporting.

The Form Is Complex and Difficult to Complete: Though it may appear daunting at first glance, the Ohio SD 101 form is straightforward once the filer understands the information required, including the employer's information, tax period, and tax due for each relevant school district.

Personal Income is Reported on SD 101: There's a misconception that personal income needs to be reported on the SD 101 form. This form is specifically for employers to report school district income tax withheld from employees' wages, not the personal income of individuals.

Corrections Cannot Be Made After Submission: Finally, many believe that once the SD 101 is submitted, no changes can be made. Corrections can indeed be submitted if an error is identified, ensuring that accurate information is reported to the state.

Understanding these misconceptions about the Ohio SD 101 form is essential for employers to comply with state tax regulations and avoid potential issues. By dispelling these myths, employers can better navigate the complexities of tax reporting and ensure timely and accurate submissions.

When filling out and using the Ohio SD 101 form, employers must ensure accuracy and timeliness to comply with state tax laws. Here are four key takeaways to remember:

Making the check payable to "SCHOOL DISTRICT INCOME TAX" and mailing it to the specified address ensures that the payment is directed to the correct state office for processing. By adhering to these guidelines, employers contribute to the efficient collection and allocation of school district income taxes, which ultimately support education within Ohio's communities.

Permanent Partial Disability Ohio - Employers are cautioned against misrepresentation of wage data, highlighting the legal implications of falsifying information on this form.

Ohio Si 7 - Information about the Ohio administrator and any changes in the position is requested.

Cdl Ohio - The program reflects an appreciation for the service and skills of military personnel in the state of Ohio.